- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

a16z 2025 Report: $40 Trillion Market Cap Milestone, The Year Global Assets Go On-chain

Original Title: State of Crypto 2025: The year crypto went mainstream

Original Authors: Daren Matsuoka, Robert Hackett, Eddy Lazzarin, Jeremy Zhang, Stephanie Zinn, a16z

Translation: xiaozou, Golden Finance

The world is undergoing full-chainization.

When we released our first crypto industry report, the field was still in its adolescence. At that time, the total crypto market value was only half of what it is today, blockchain was slower, more costly, and less stable.

Over the past three years, crypto builders have weathered market crashes and policy uncertainties but have continued to drive significant upgrades to infrastructure and technological breakthroughs. These efforts have brought us to the present moment—crypto assets are becoming a historic part of the modern economy.

The main theme of crypto in 2025 is industry maturation. In short, the crypto world has grown up:

Traditional financial giants (Visa, BlackRock, Fidelity, JPMorgan) and tech-native challengers (PayPal, Stripe, Robinhood) have all launched crypto products;

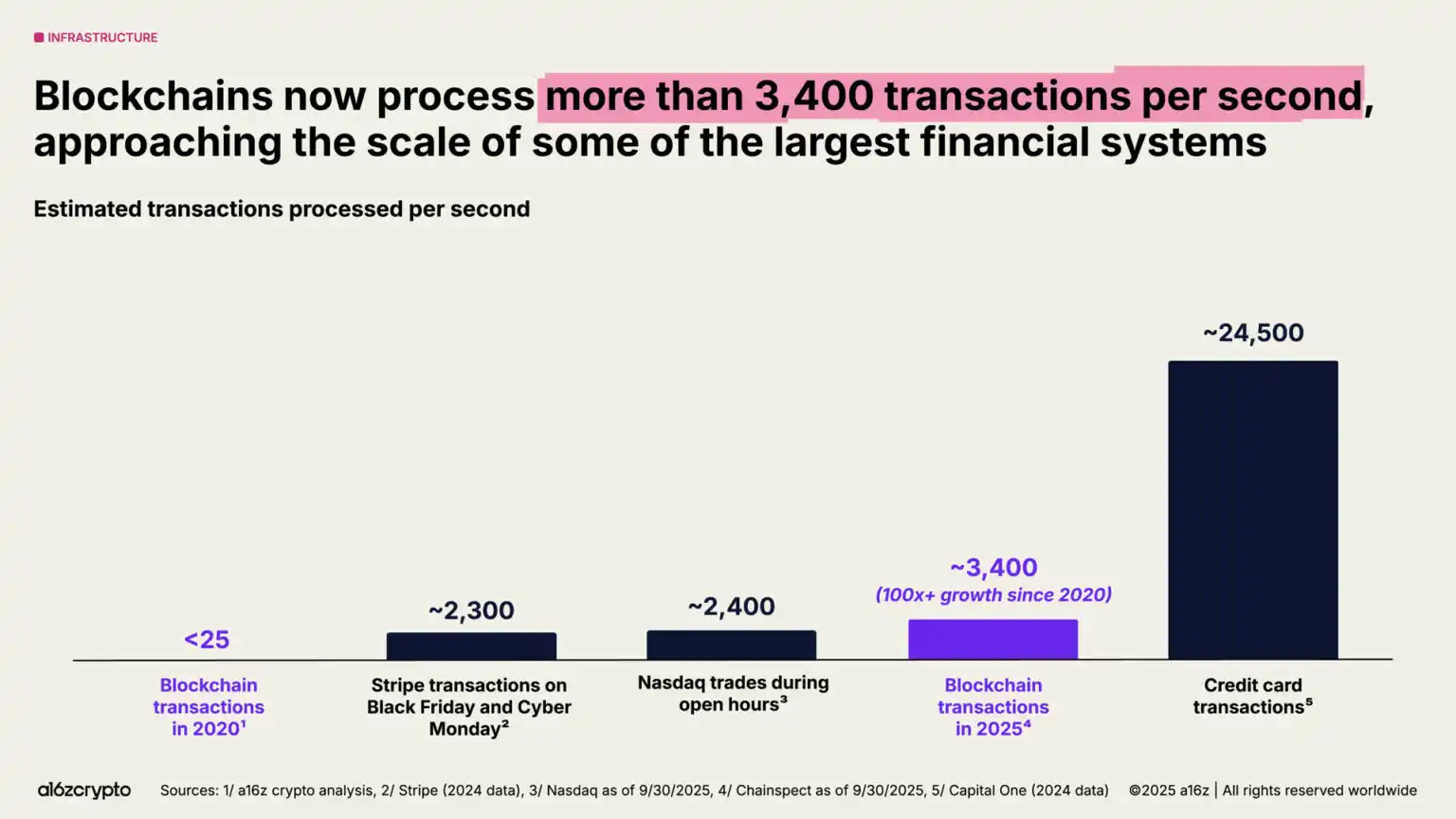

Blockchain's transaction processing per second has exceeded 3,400 transactions (a growth of over a hundredfold in five years);

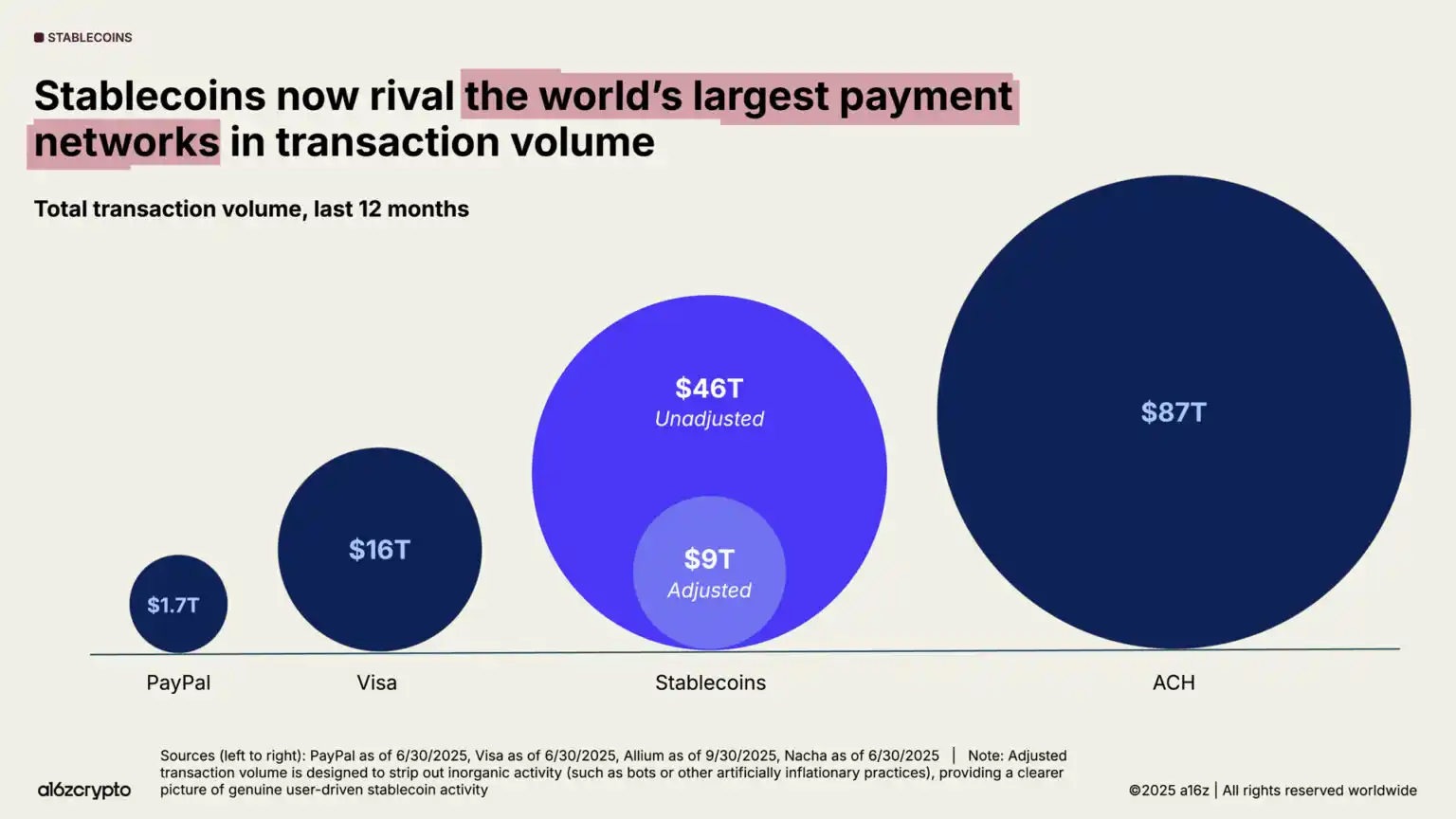

Stablecoins support an annual transaction volume of $46 trillion (adjusted to $9 trillion), on par with Visa and PayPal;

Bitcoin and Ethereum exchange-traded product volumes have exceeded $175 billion.

This year's report delves deep into industry transformation: from institutional adoption and the rise of stablecoins to the integration of crypto with artificial intelligence. We are introducing a crypto data dashboard for the first time, tracking industry evolution through key metrics.

The following are the key points of this article:

· The crypto market has taken on a scalable, global, and continually growing trend;

· Financial institutions have fully embraced crypto assets;

· Stablecoins Enter Mainstream Adoption;

· US Crypto Ecosystem Resilience Reaches an All-Time High;

· Global Acceleration of On-Chain Processes;

· Blockchain Infrastructure Approaches a Maturity Inflection Point;

· Deep Integration of Cryptocurrency and Artificial Intelligence Technologies.

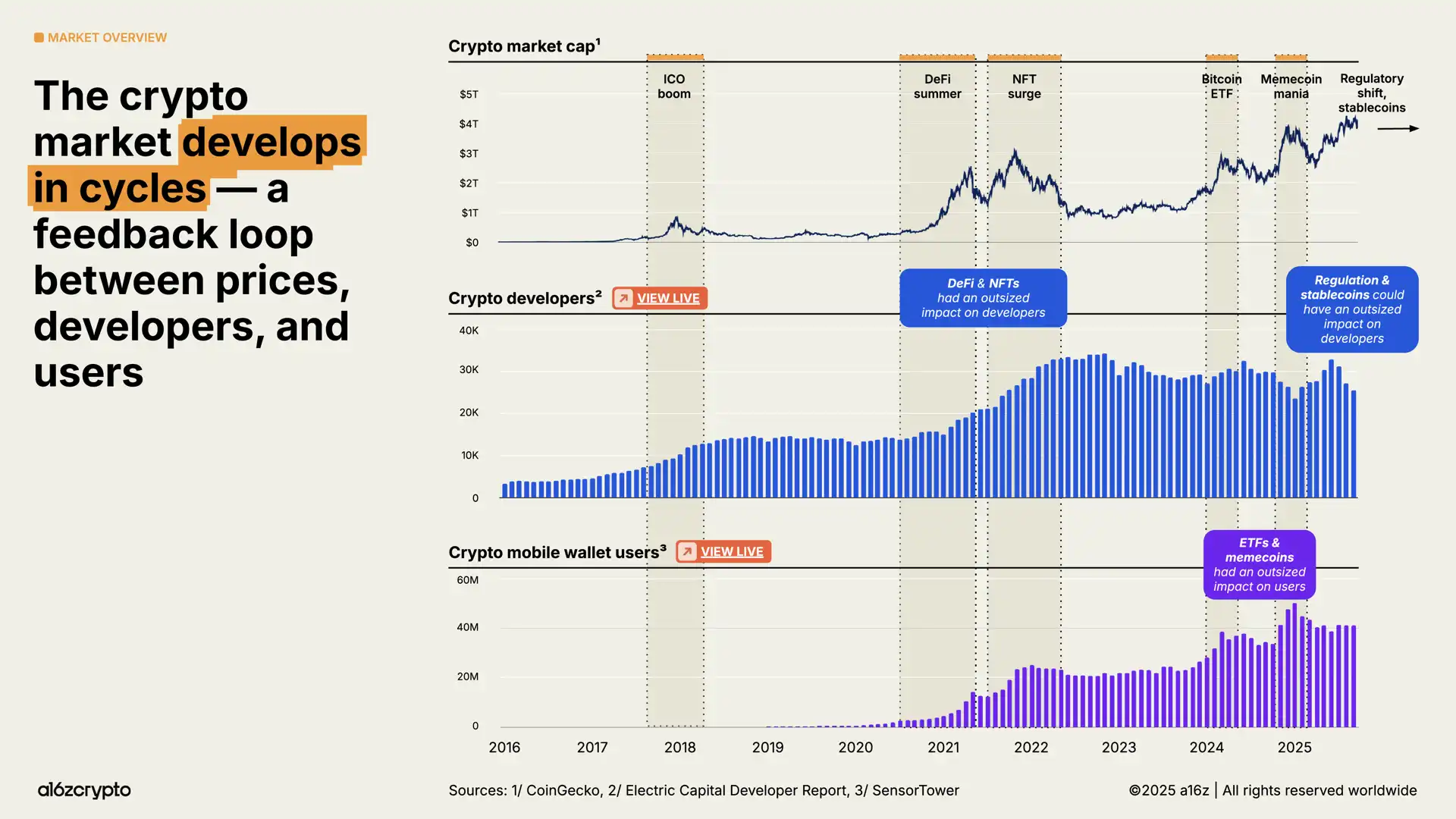

1. The Crypto Market Has Formed a Scalable, Global, and Continuously Growing Trend

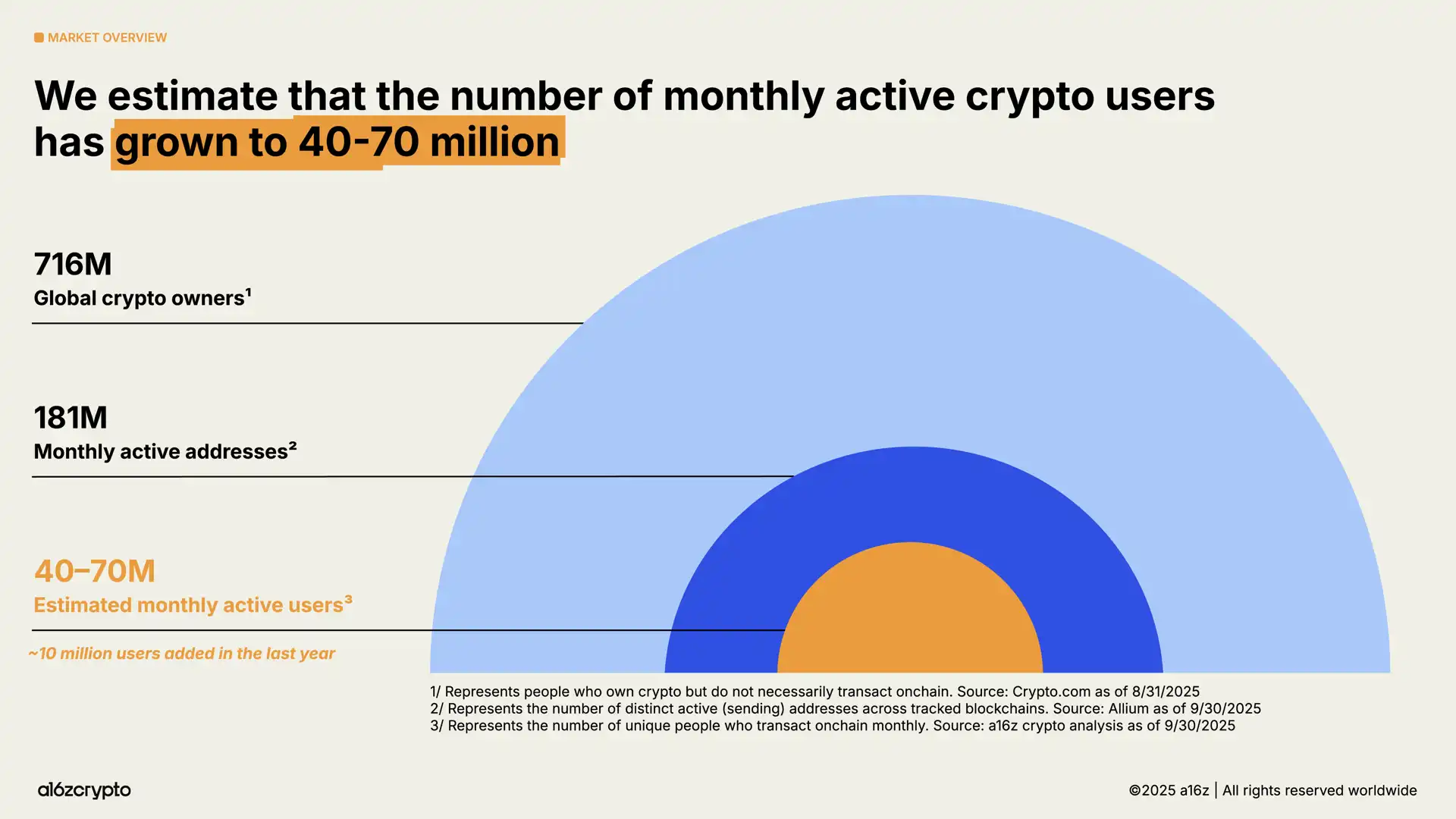

By 2025, the total crypto market capitalization has surpassed the $4 trillion mark for the first time, demonstrating the industry's overall leap. The number of mobile crypto wallet users has surged by 20% year-on-year, reaching a historic high. From a regulatory pushback to a policy-supportive environment shift, coupled with the accelerated implementation of technologies such as stablecoins and tokenization of traditional financial assets, will define the trajectory of the next cycle of development.

Based on our analysis using an updated methodology, the current global active crypto users are estimated to be around 40 to 70 million, an increase of about 10 million from last year.

This number represents only a small proportion of the 716 million crypto asset holders globally (a 16% increase year-on-year) and is also much lower than the approximately 181 million on-chain monthly active addresses (an 18% decrease year-on-year).

The difference in numbers between passive holders (those who own crypto assets but do not engage in on-chain transactions) and active users (those who regularly transact on-chain) reveals an important opportunity for crypto builders: how to reach the potential user base that already holds crypto assets but has not yet participated in on-chain activities.

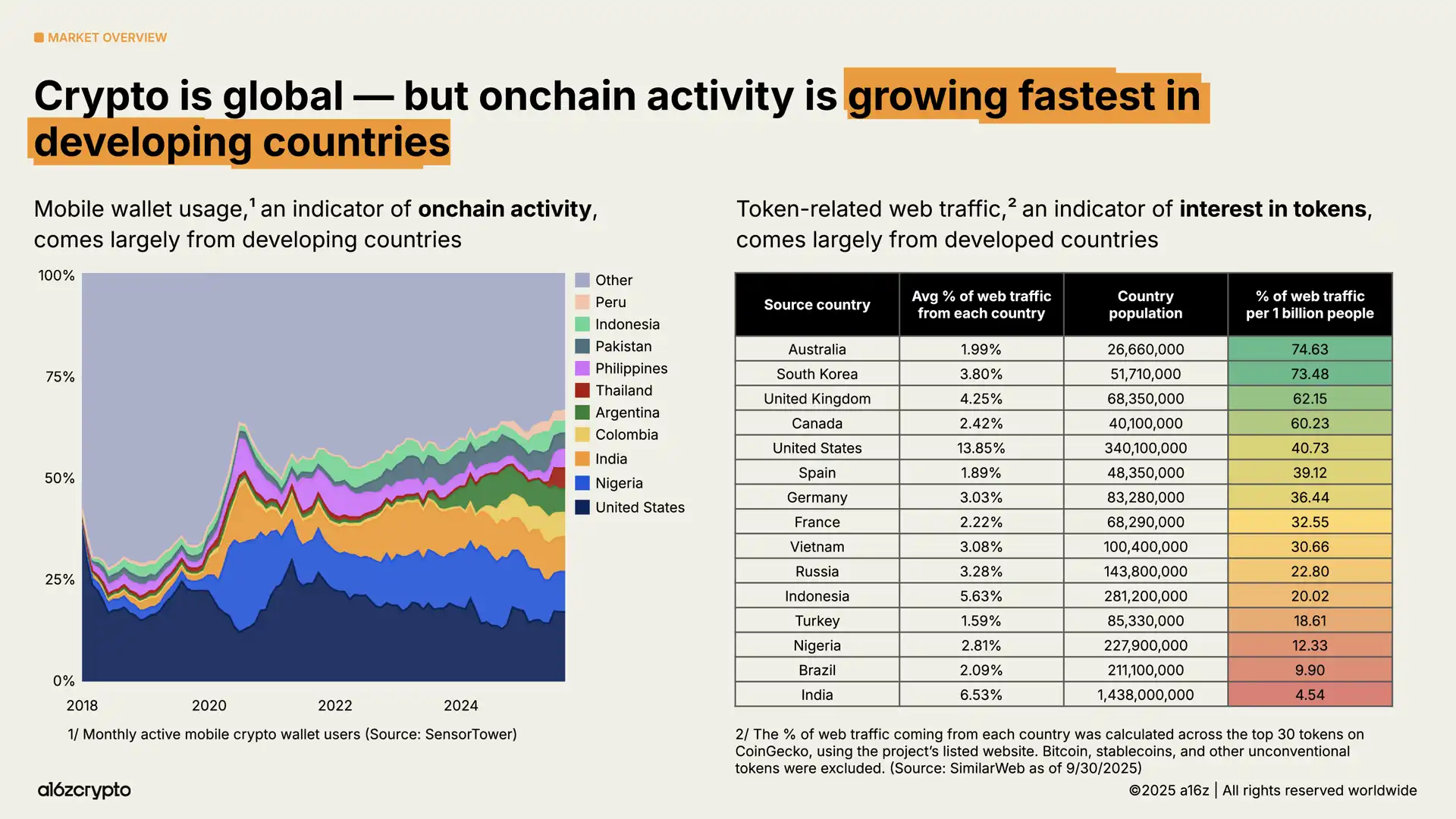

So, where are these crypto users distributed? What activities are they engaged in?

The crypto ecosystem has a global nature, but different regions exhibit differentiated usage patterns. The usage of mobile wallets, as an indicator of on-chain activities, is growing fastest in emerging markets such as Argentina, Colombia, India, and Nigeria (especially Argentina, where the use of crypto mobile wallets has increased 16-fold against the backdrop of a currency crisis intensifying over the past three years).

Meanwhile, our analysis of the geographical sources of token-related network traffic shows that the token interest index leans more toward developed countries. Compared to user behavior in developing countries, activities in countries like Australia and South Korea may be more concentrated in trading and speculation.

Bitcoin (still accounting for over half of the total cryptocurrency market value) has been favored by investors as a store of value, reaching a historic high of over $126,000. Meanwhile, Ethereum and Solana have recaptured most of their lost ground following the 2022 crash.

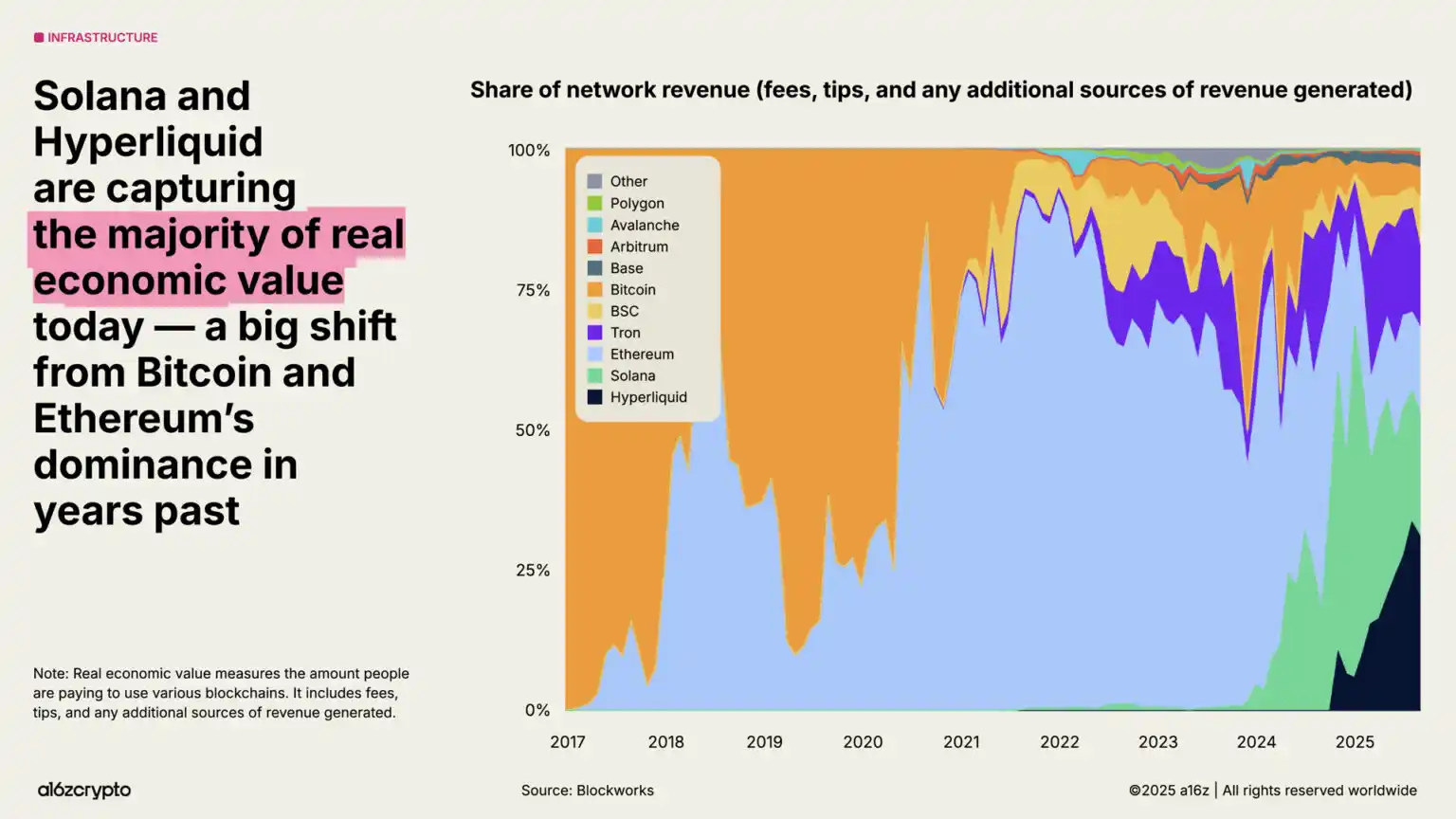

As blockchain continues to scale, the fee market matures, and new applications emerge, certain metrics are becoming increasingly important. One of these is "real economic value" – measuring the actual scale of fees users pay to use the blockchain. Currently, Hyperliquid and Solana account for 53% of revenue-generating economic activity, marking a significant shift from the previous dominance of Bitcoin and Ethereum.

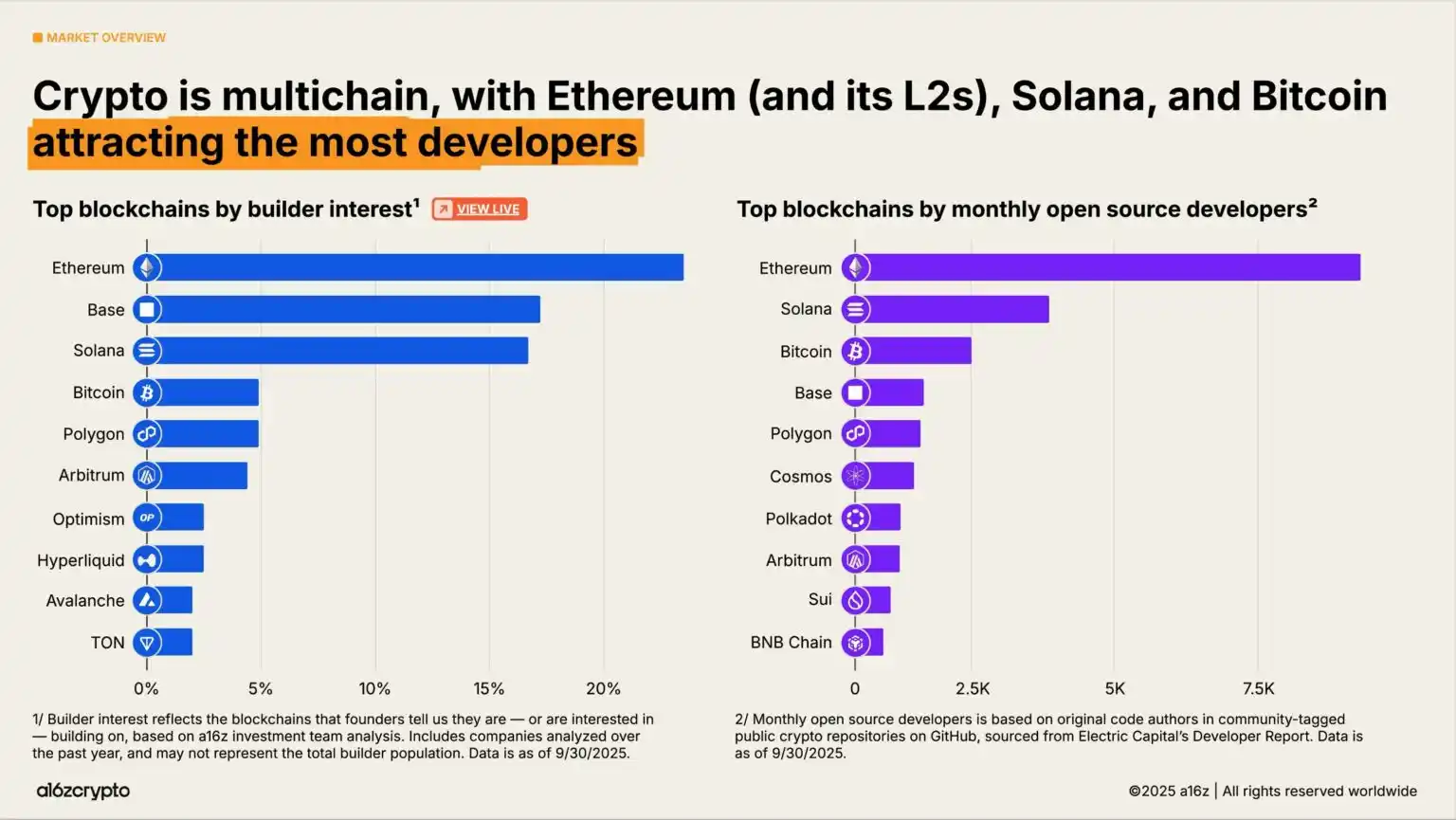

From the developer ecosystem perspective, the crypto world still exhibits a multi-chain landscape, with Bitcoin, Ethereum and its layer 2 networks, and Solana forming the three core developer hubs. By 2025, Ethereum and its layer 2 networks have become the top choice for new developers, while Solana is one of the fastest-growing ecosystems – with developer interest increasing by 78% over the past two years. This data is derived from analysis by the a16z crypto investment team on entrepreneurs' preferred development platforms.

2. Financial Institutions Fully Embrace Cryptocurrency Assets

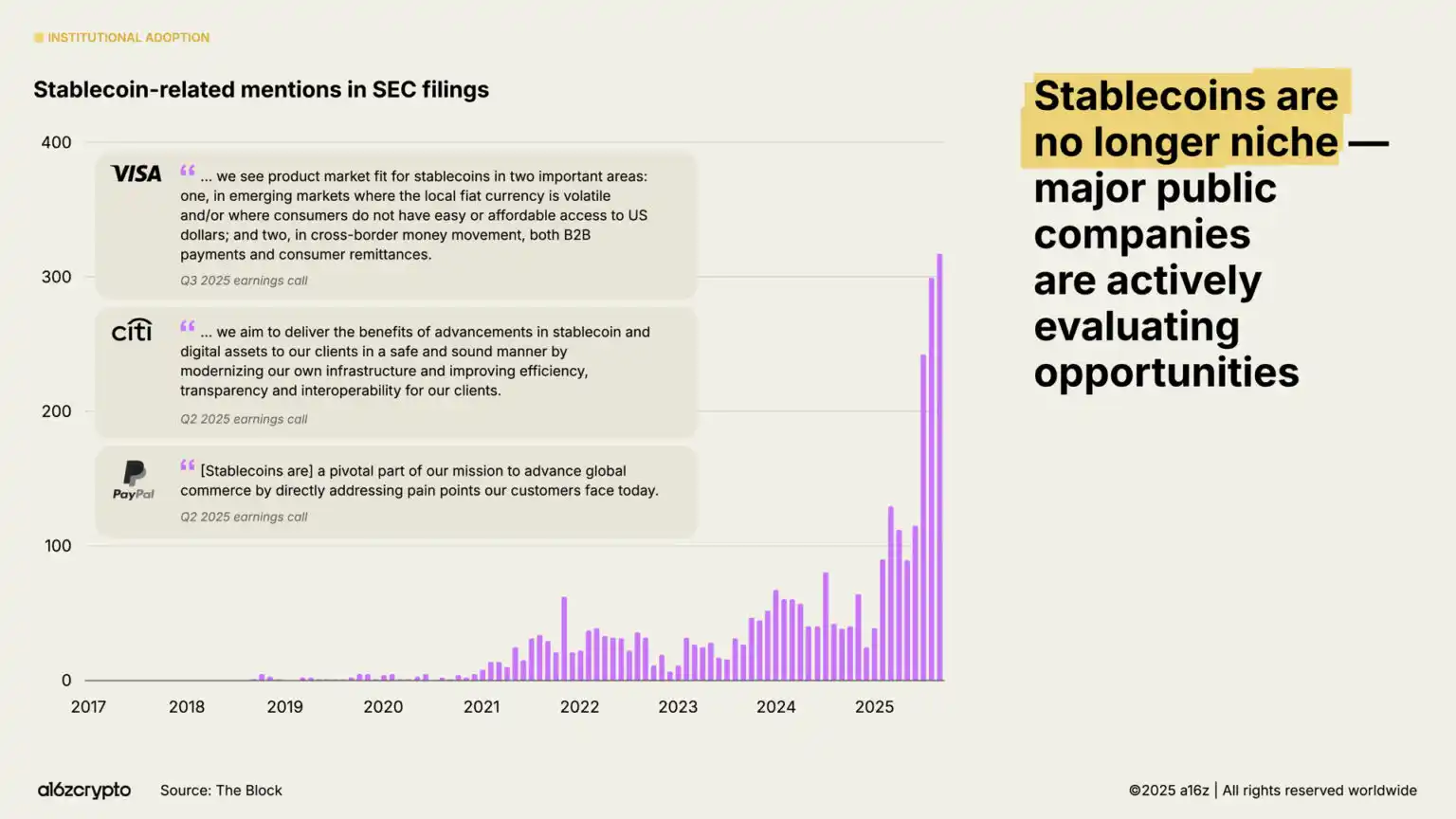

2025 can be described as the year of institutional adoption. Following last year's "Cryptocurrency Industry Landscape" report, which declared stablecoins achieved product-market fit in just five days, Stripe announced the acquisition of the stablecoin infrastructure platform Bridge, kicking off the traditional financial companies' public positioning in the stablecoin space.

Months later, Circle's multibillion-dollar IPO marked stablecoin issuers officially entering the mainstream financial institution realm. Subsequently, in July, the bipartisan-supported "GENIUS Act" was formally legislated, providing clear action guidance for builders and institutions. The frequency of stablecoin mentions in SEC filings grew by 64%, and announcements of strategic moves by major financial institutions surged.

Institutional adoption is gaining momentum. Traditional financial institutions such as Citigroup, Fidelity, JPMorgan Chase, Mastercard, Morgan Stanley, and Visa have started (or are planning) to directly offer crypto products to consumers, enabling them to buy, sell, and hold digital assets as well as stocks, exchange-traded products, and other traditional instruments. Meanwhile, platforms like PayPal and Shopify are doubling down on the payment space, building infrastructure for everyday transactions between merchants and consumers.

Aside from direct product offerings, major fintech companies like Circle, Robinhood, and Stripe are actively developing or have announced plans to develop new blockchains focused on payments, real-world assets, and stablecoins. These initiatives may drive more payment flows onto the blockchain, promote enterprise adoption, and ultimately build a larger, faster, more globalized financial system.

These companies possess vast distribution networks. With continued development, cryptographic technology is poised to be fully integrated into the financial services we use in our daily lives.

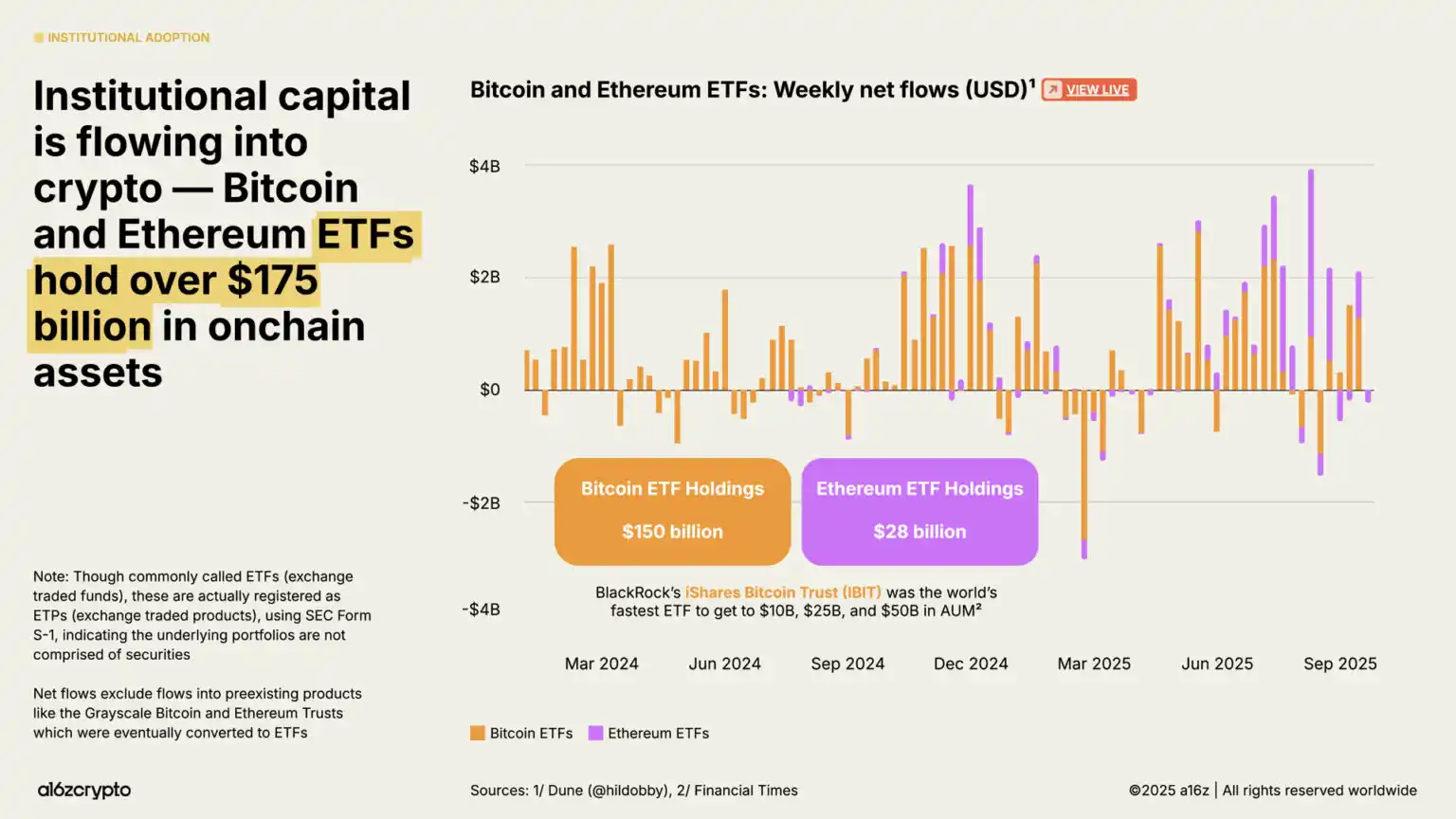

Exchange-traded products have become another key driver of institutional investment, with the current on-chain crypto asset holdings surpassing $175 billion, a 169% surge from $65 billion a year ago.

BlackRock's iShares Bitcoin Trust is hailed as the most actively traded bitcoin exchange-traded product in history, and the recently launched Ethereum exchange-traded product has also seen significant inflows in recent months. (Note: Although commonly referred to as exchange-traded funds, these products are actually filed under an S-1 registration with the SEC as exchange-traded products, indicating that their underlying assets do not include securities.)

These products have significantly lowered the investment barrier for crypto assets, opening up an entry point for institutional capital that has historically remained on the industry's periphery.

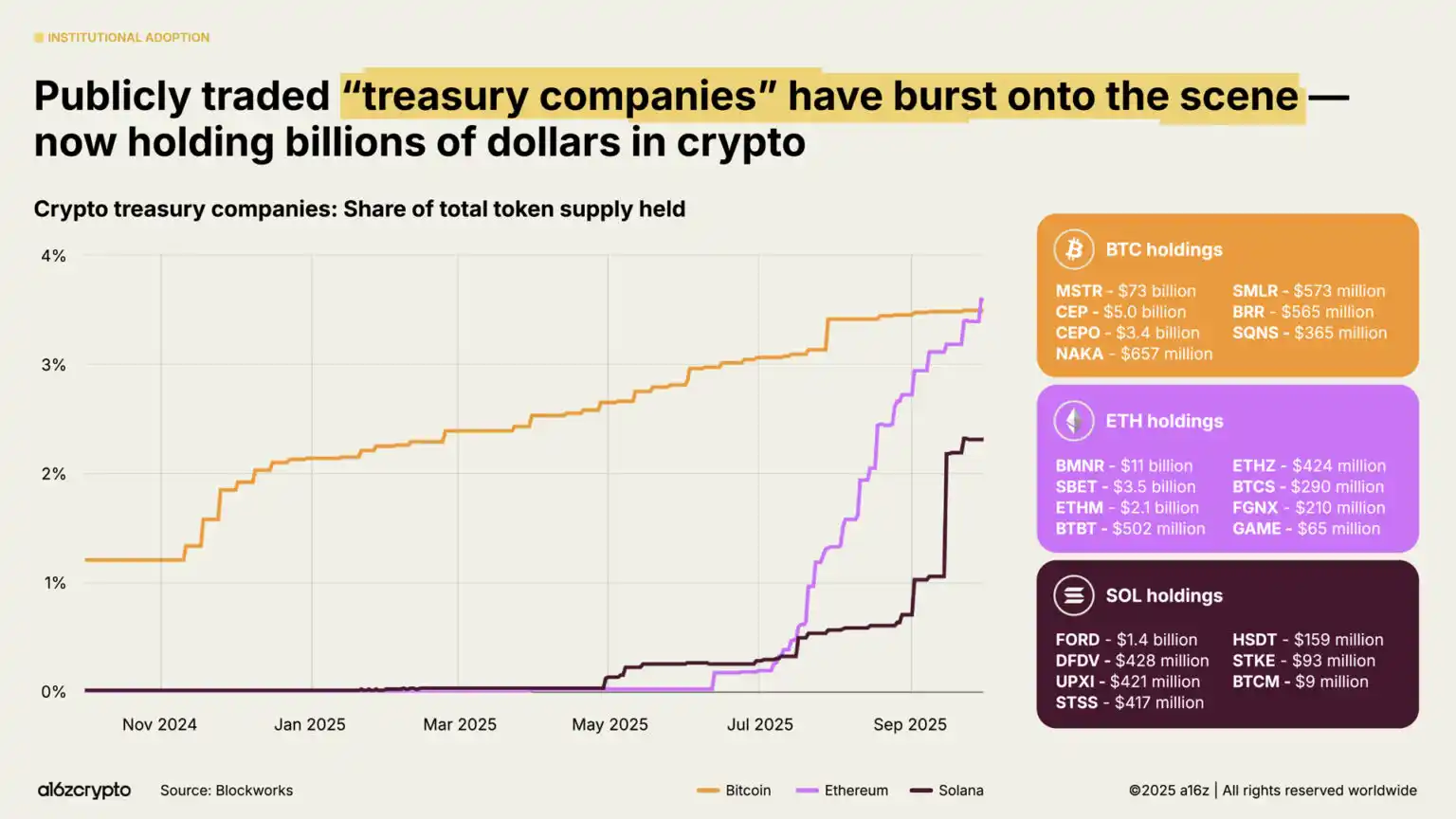

Publicly traded "digital asset reserve" companies—entities that hold crypto assets on their balance sheets (similar to a corporate treasury holding cash)—currently collectively hold approximately 4% of the circulating supply of Bitcoin and Ethereum. These digital asset reserve companies, combined with exchange-traded products, now hold around 10% of the circulating supply of Bitcoin and Ethereum.

3. Mainstreaming of Stablecoins

The most significant sign of the maturity of the crypto market in 2025 is undoubtedly the rise of stablecoins. In previous years, stablecoins were mainly used for settling speculative crypto trades, but in the last two years, they have become the fastest and cheapest way for global transfers in USD — processing millions of transactions per second, with a cost of less than one cent per transaction, covering the vast majority of regions globally.

This year, stablecoins have become a cornerstone of the on-chain economy.

Over the past year, the total stablecoin transaction volume reached $46 trillion, a 106% year-on-year increase. While this mainly represents fund flows (unlike retail payments through card networks), the scale has now reached three times that of Visa and is nearing the ACH network that spans the entire US banking system.

When adjusted (excluding bot and artificially inflated transaction data), the real stablecoin transaction volume over the past 12 months was $9 trillion, an 87% year-on-year growth, which is over five times PayPal's volume and surpasses half of Visa's scale.

Adoption is accelerating. The adjusted monthly stablecoin transaction volume has surged to a historic high, with nearly $1.25 trillion just in September 2025.

Of note, this activity has a relatively low correlation with the overall crypto trading volume — indicating that stablecoins are being used for non-speculative purposes. More importantly, this confirms the alignment of its product with the market.

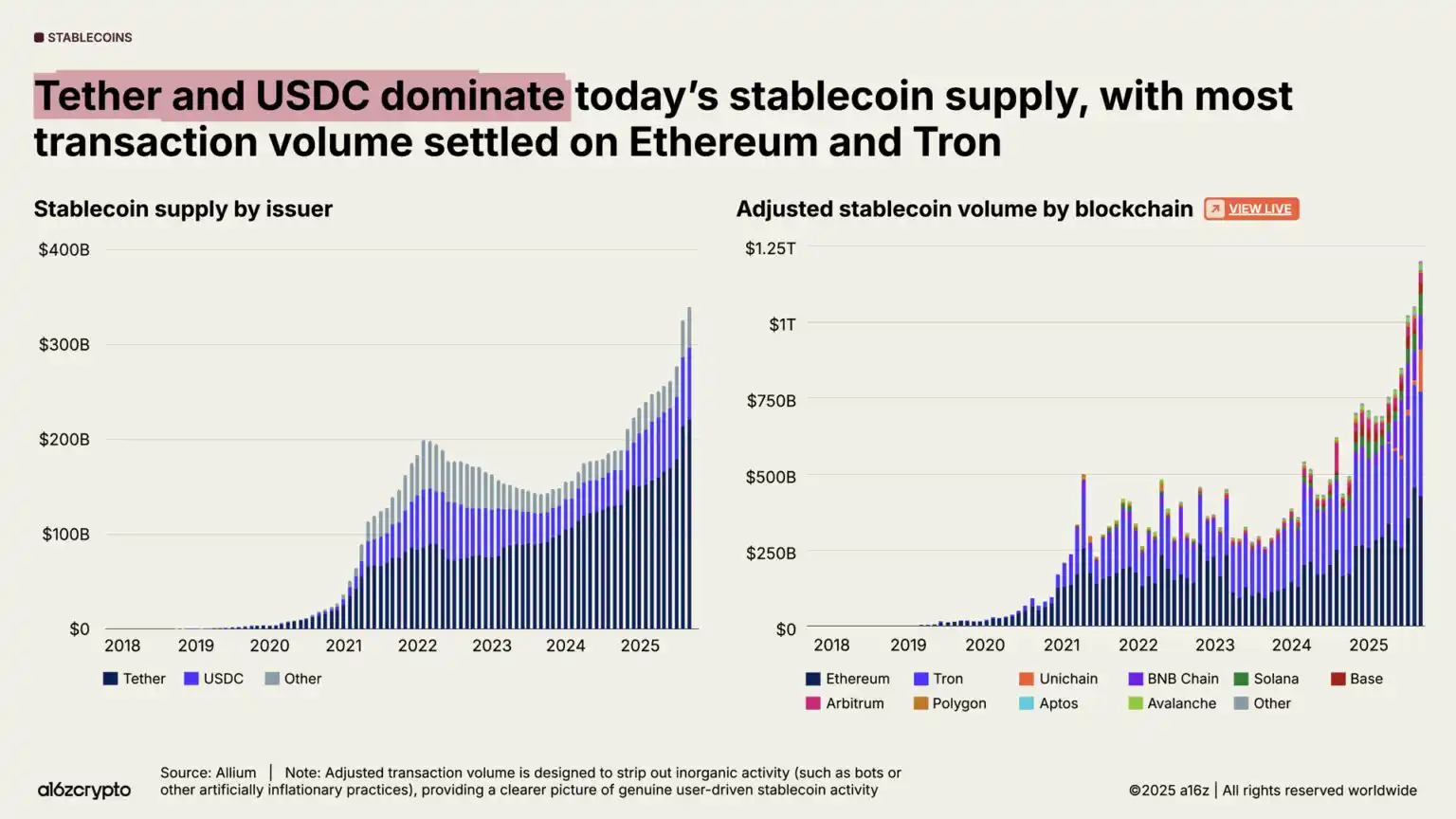

The total stablecoin supply has also reached a historic high, now exceeding $300 billion.

The market is dominated by leading stablecoins: Tether and USDC account for 87% of the total supply. In September 2025, the stablecoin transaction volume processed on the Ethereum and Tron blockchains (when adjusted) reached $772 billion, representing 64% of all transaction volume. While these two major issuers and blockchains hold the lion's share of stablecoin activity, the momentum of growth for emerging blockchains and issuers is also accelerating.

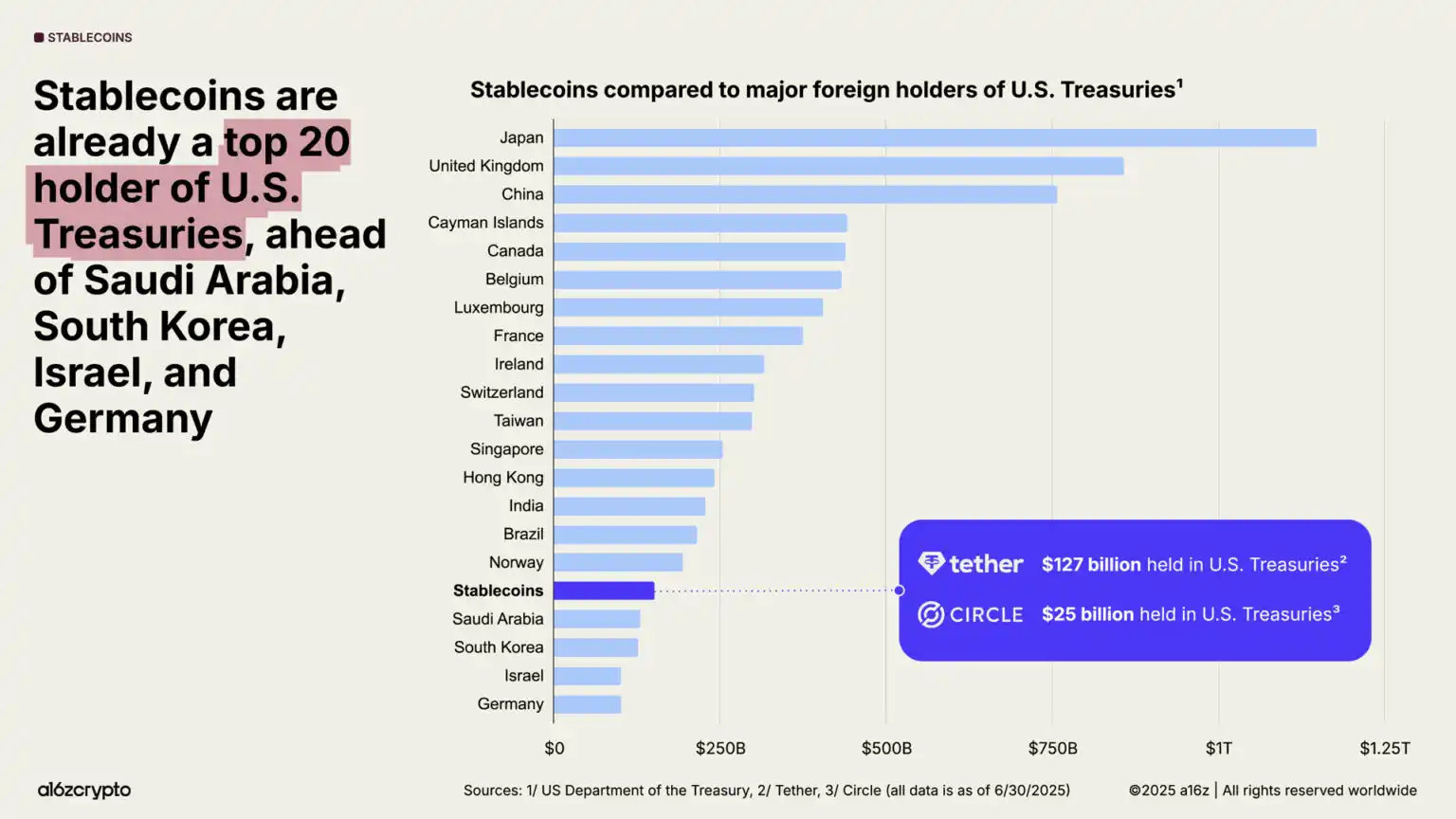

Stablecoins have become a significant force in the global macroeconomy: over 1% of the USD exists in tokenized stablecoin form on public blockchains, and their holdings of US Treasury bonds have risen from 20th place last year to 17th place. Currently, stable coins collectively hold over $150 billion in US Treasuries — surpassing the holdings of many sovereign nations.

Meanwhile, despite a weakening global demand for U.S. Treasuries, its national debt continues to soar. For the first time in 30 years, foreign central banks' gold reserves have exceeded U.S. Treasury holdings.

However, stablecoins are on the rise: over 99% of stablecoins are dollar-denominated, and their market is expected to grow more than tenfold to over $30 trillion by 2030. This could potentially provide a robust and sustainable source of demand for U.S. debt in the coming years.

Even as foreign central banks reduce their holdings of U.S. debt, stablecoins are solidifying the dollar's dominance.

4. Resilience of the U.S. Cryptocurrency Ecosystem Reaches an All-Time High

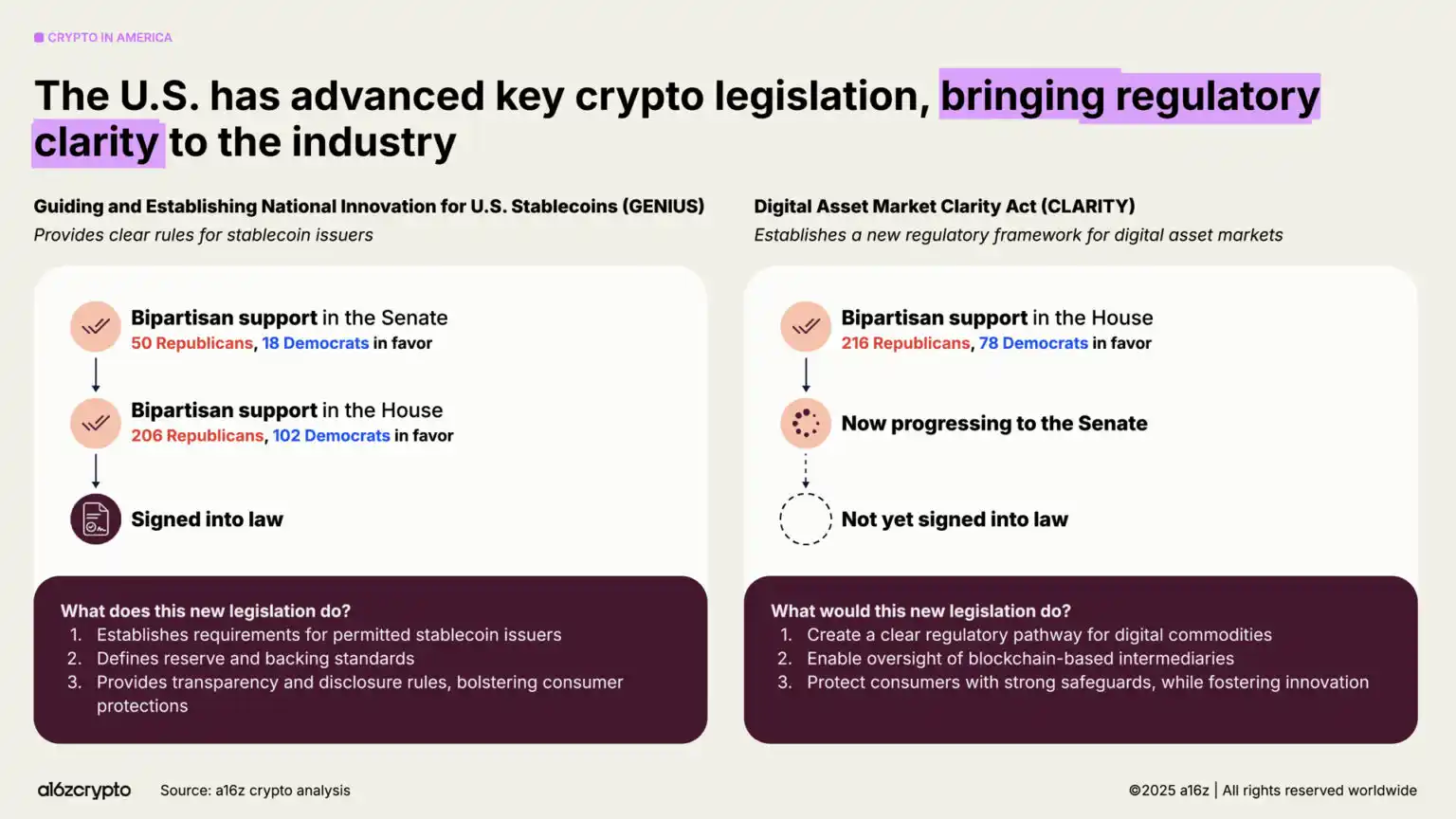

The U.S. has reversed its previous hostile stance towards the cryptocurrency sector, revitalizing builder confidence.

This year, the passage of the "GENIUS Act" and approval of the "CLARITY Act" by the House of Representatives signal a bipartisan consensus that cryptocurrency assets will not only survive in the U.S., but also have the conditions for prosperous development. These two acts together establish a stablecoin regulatory framework that balances innovation and investor protection, market structure, and digital asset supervision. Meanwhile, Executive Order 14178 revokes previous anti-crypto directives and establishes an inter-agency working group to drive the modernization of federal digital asset policy.

The regulatory environment is paving the way for builders to fully unleash the potential of tokens as a new digital lingua franca, much like the significance of websites to earlier generations of the internet. With a clearer regulatory framework, more network tokens will complete the economic loop by generating returns for holders, thus creating a new economic engine for the internet that is self-sustaining and allows more users to share in the system's rewards.

5. Global Acceleration of On-Chain Transformation

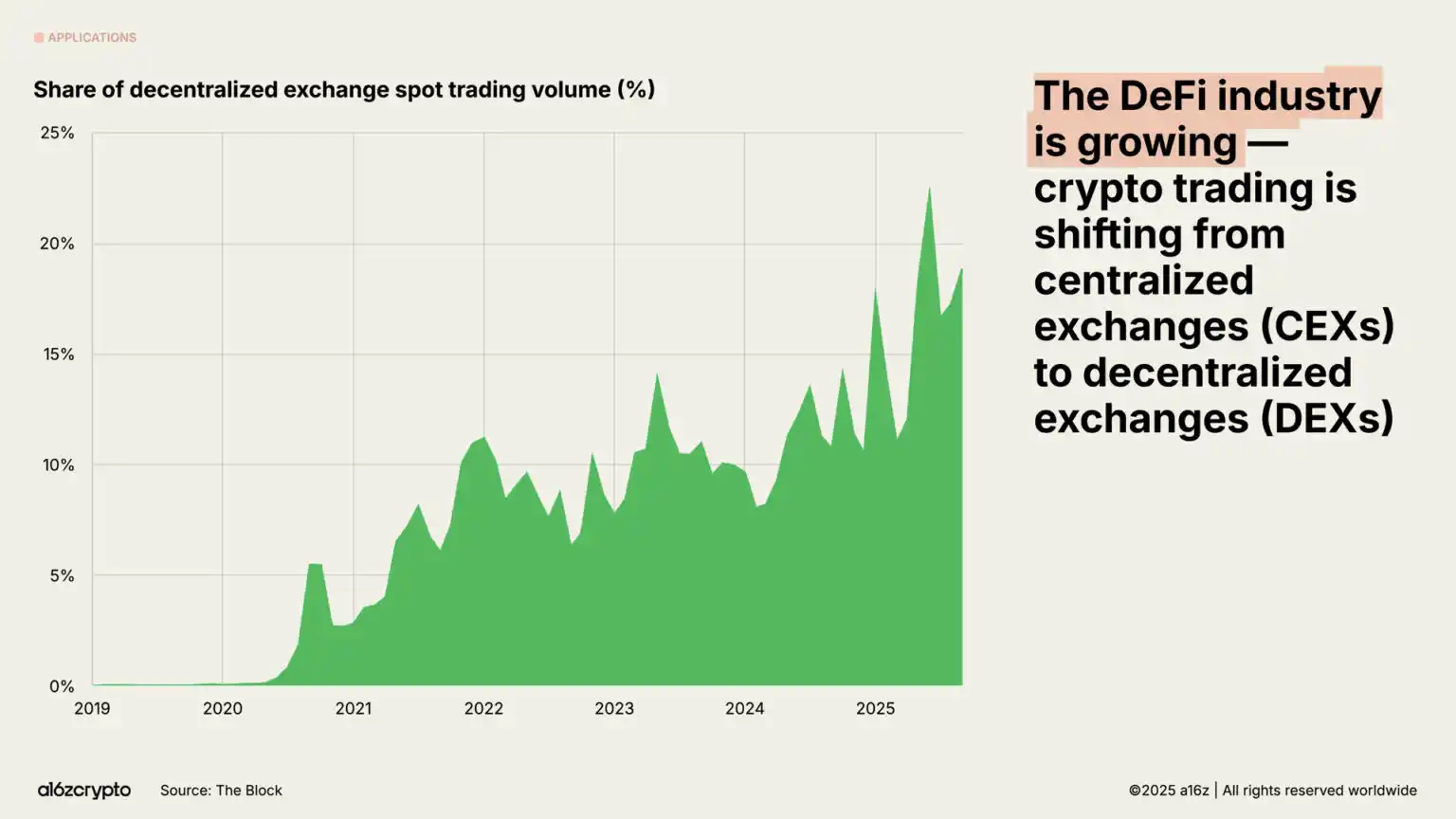

What was once a niche experimental ground for early adopters, the on-chain economy has evolved into a diverse ecosystem with tens of millions of monthly active participants. Today, nearly one-fifth of spot trading volume is conducted through decentralized exchange platforms.

The trading volume of perpetual contracts has surged nearly 8x in the past year, experiencing explosive growth among cryptocurrency speculators. Decentralized perpetual contract trading platforms such as Hyperliquid have processed trillions of dollars in trading volume, generating over $1 billion in annualized revenue this year—data that is now comparable to some centralized exchanges.

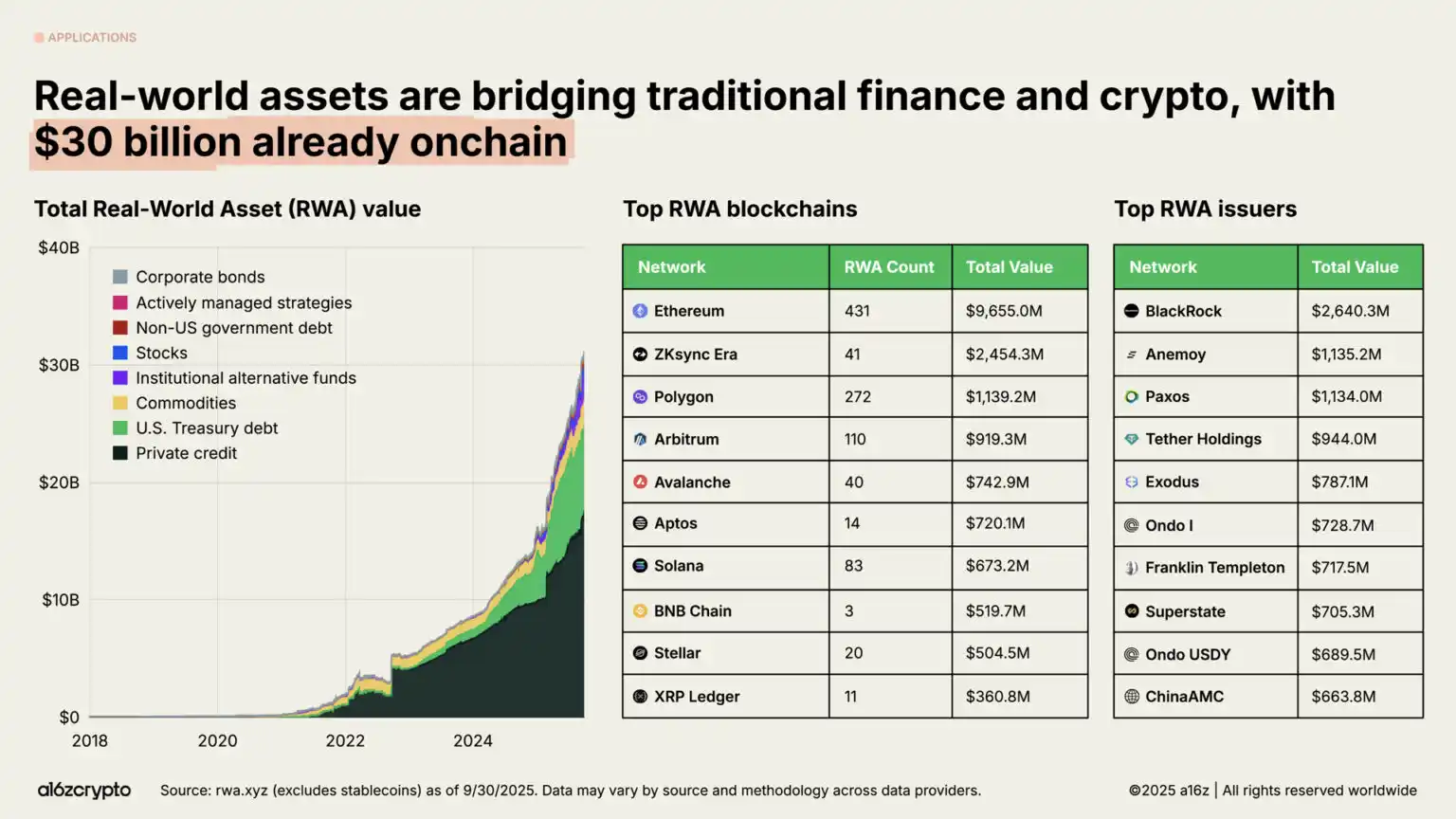

Real-world assets—including U.S. Treasuries, money market funds, private credit, and real estate tokenized as traditional assets on-chain—are bridging the gap between crypto and traditional finance. The total market size of tokenized RWAs has reached $30 billion, nearly quadrupling over the past two years.

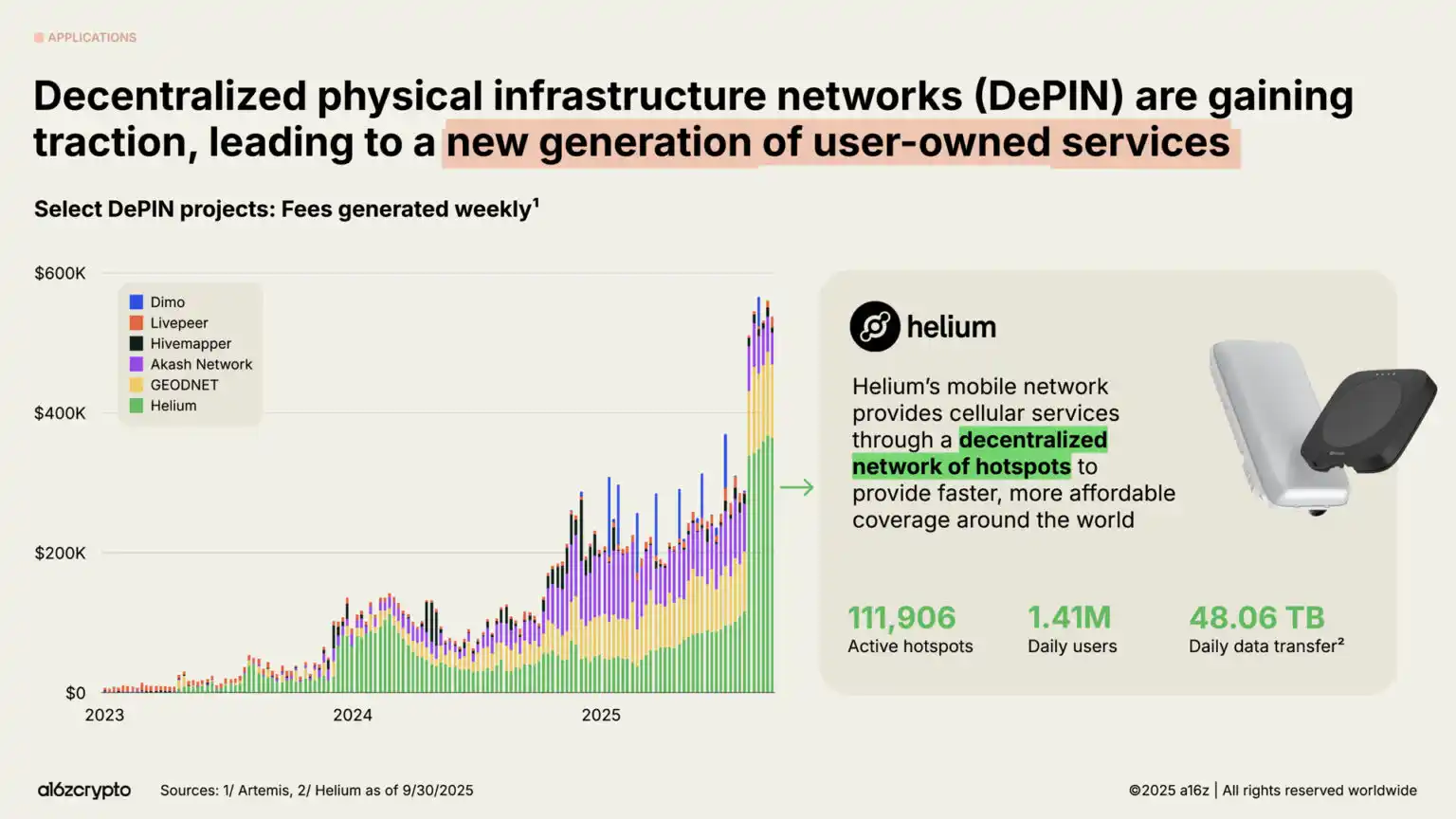

Outside the financial sector, the most ambitious frontier of blockchain by 2025 lies in DePIN—decentralized Physical Infrastructure Network.

Just as DeFi is restructuring the financial system, DePIN is reshaping physical infrastructure such as telecom networks, transportation systems, and energy grids. This field holds immense potential: the World Economic Forum predicts the DePIN market size will reach $35 trillion by 2028.

The Helium network serves as the most representative case. This grassroots-driven wireless network, operated by over 111,000 users through hotspots, currently provides 5G cellular coverage to 1.4 million daily active users.

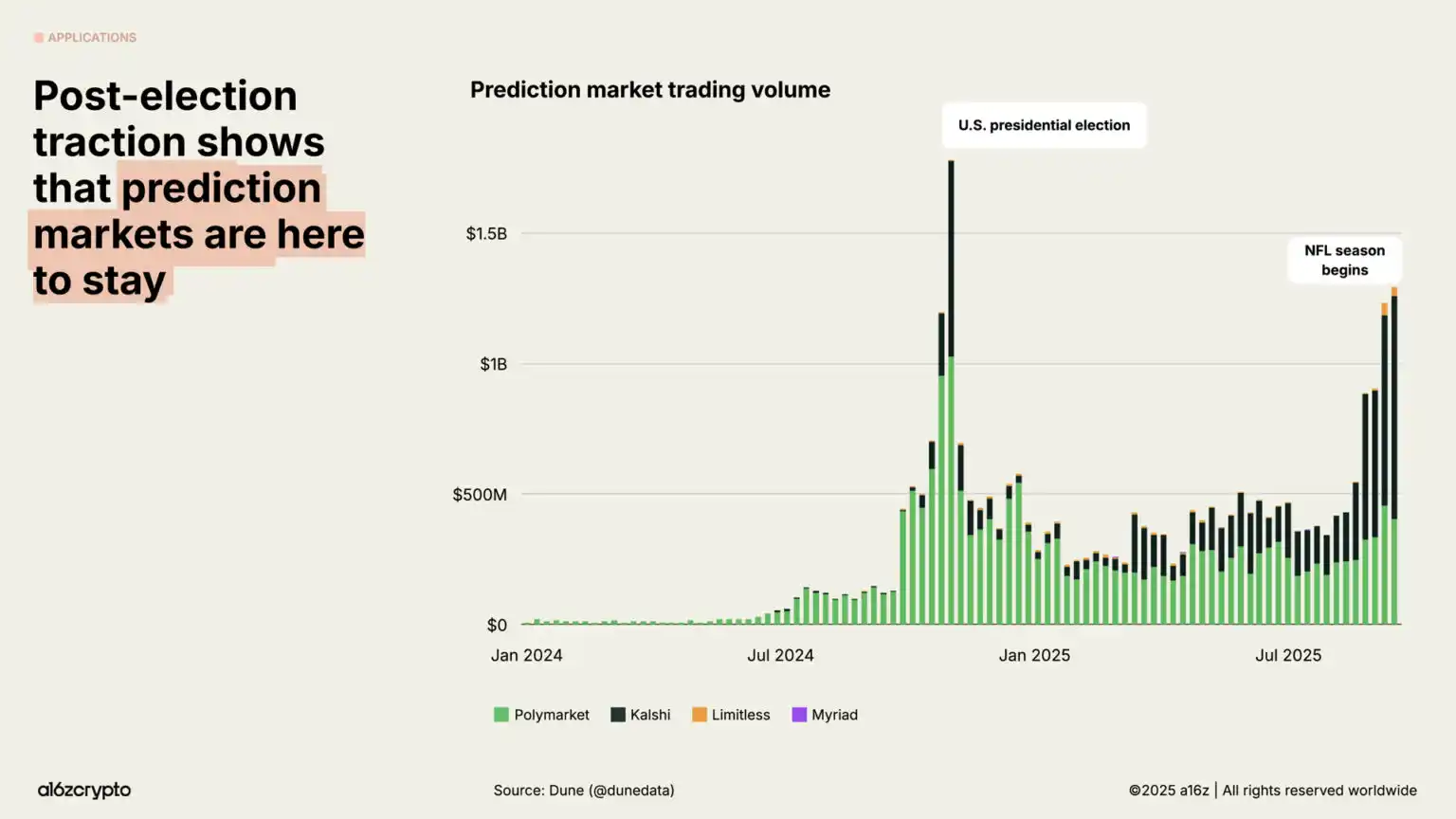

In 2024, the prediction market is set to break into the mainstream during the U.S. presidential election cycle, with leading platforms such as Polymarket and Kalshi seeing monthly trading volumes in the billions of dollars. Despite past doubts about "maintaining activity in non-election years," these platforms have seen nearly a 5x increase in trading volume since early 2025, approaching historical highs.

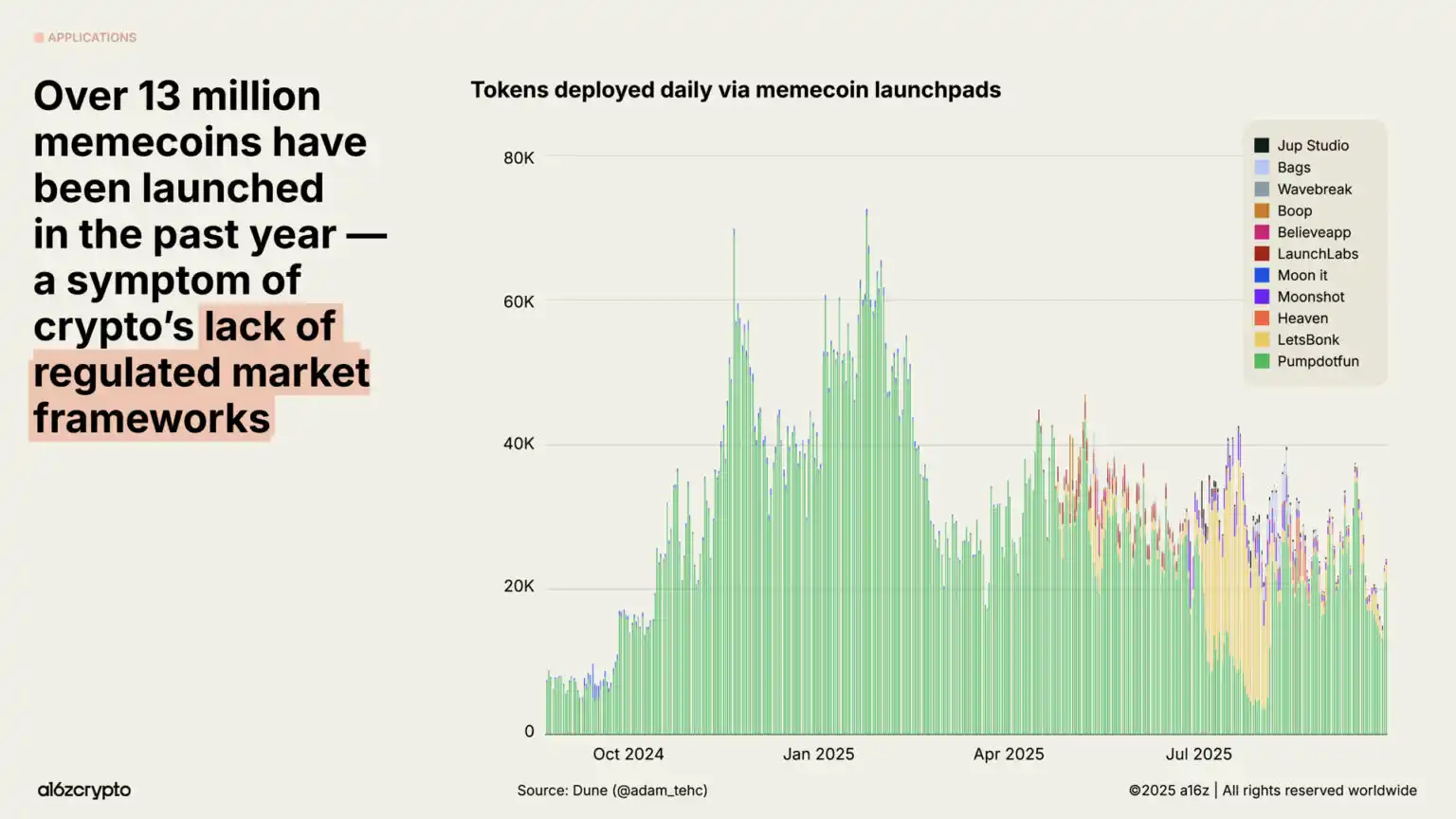

In an environment lacking clear regulation, Memecoins have experienced explosive growth, with over 13 million varieties emerging in the past year. As benign policies and bipartisan legislation clear the way for more constructive blockchain use cases, this trend has cooled off in recent months—September issuance has dropped by 56% compared to January.

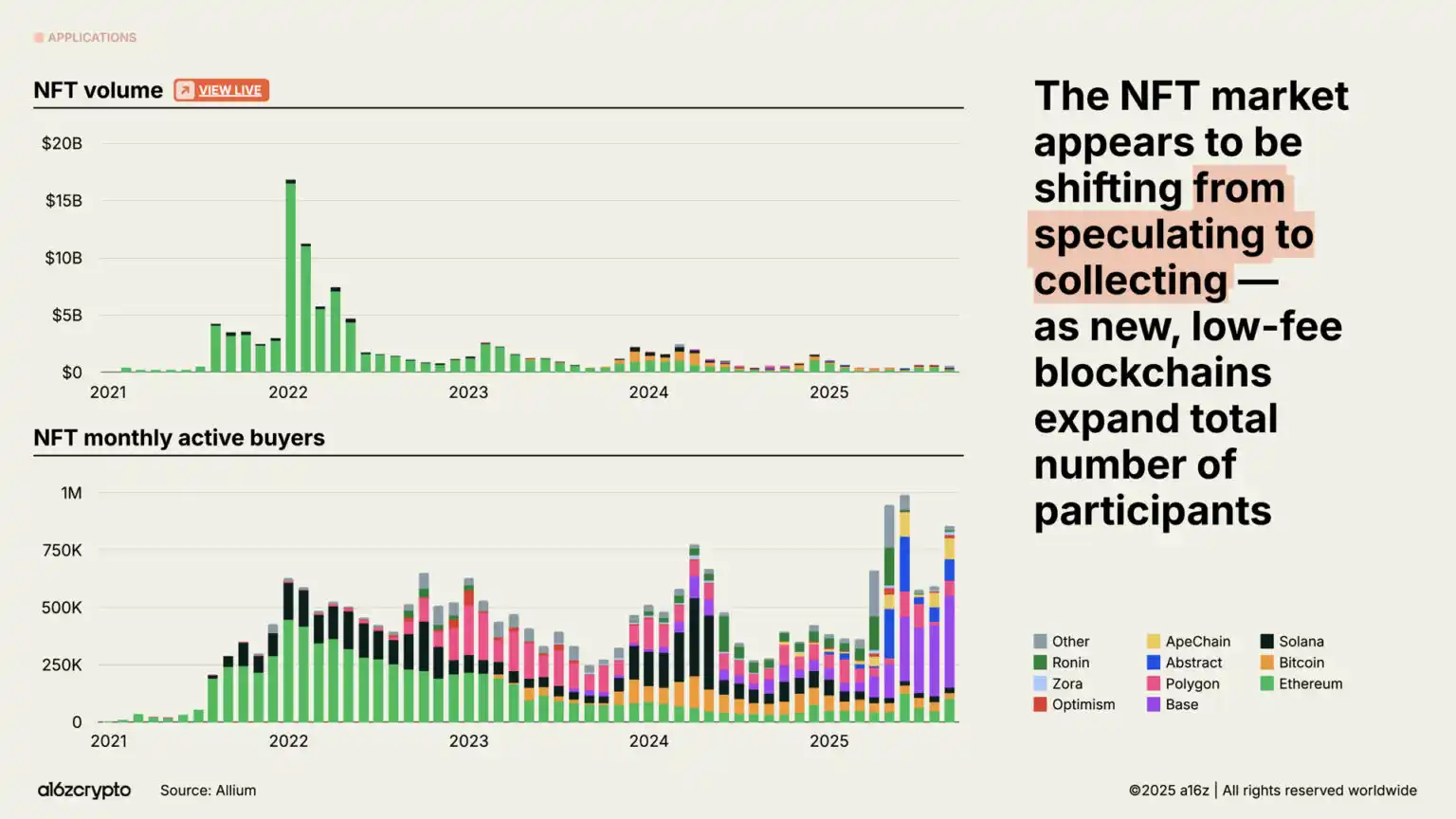

Although the NFT market trading volume has not returned to the peak of 2022, the monthly active buyer count continues to grow. These trends seem to indicate that consumer behavior is shifting from speculation to collecting, with the lower block space costs on chain layers like Solana and Base facilitating this.

6. Blockchain Infrastructure Approaching Maturity Inflection Point

Without significant advances in blockchain infrastructure, none of these activities would be possible.

In just five years, the total transaction throughput of mainstream blockchain networks has grown over 100 times. The blockchain's transaction processing capacity per second has increased from less than 25 transactions to 3400 transactions per second, now on par with the Nasdaq transaction speed and Stripe's global processing volume during Black Friday, at a cost that is only a fraction of historical costs.

Within the blockchain ecosystem, Solana has become one of the most prominent representatives. Its high-performance, low-cost architecture now supports various applications from the DePIN project to the NFT market, with its native apps generating $3 billion in revenue over the past year. Planned upgrades are expected to double the network's capacity by the end of the year.

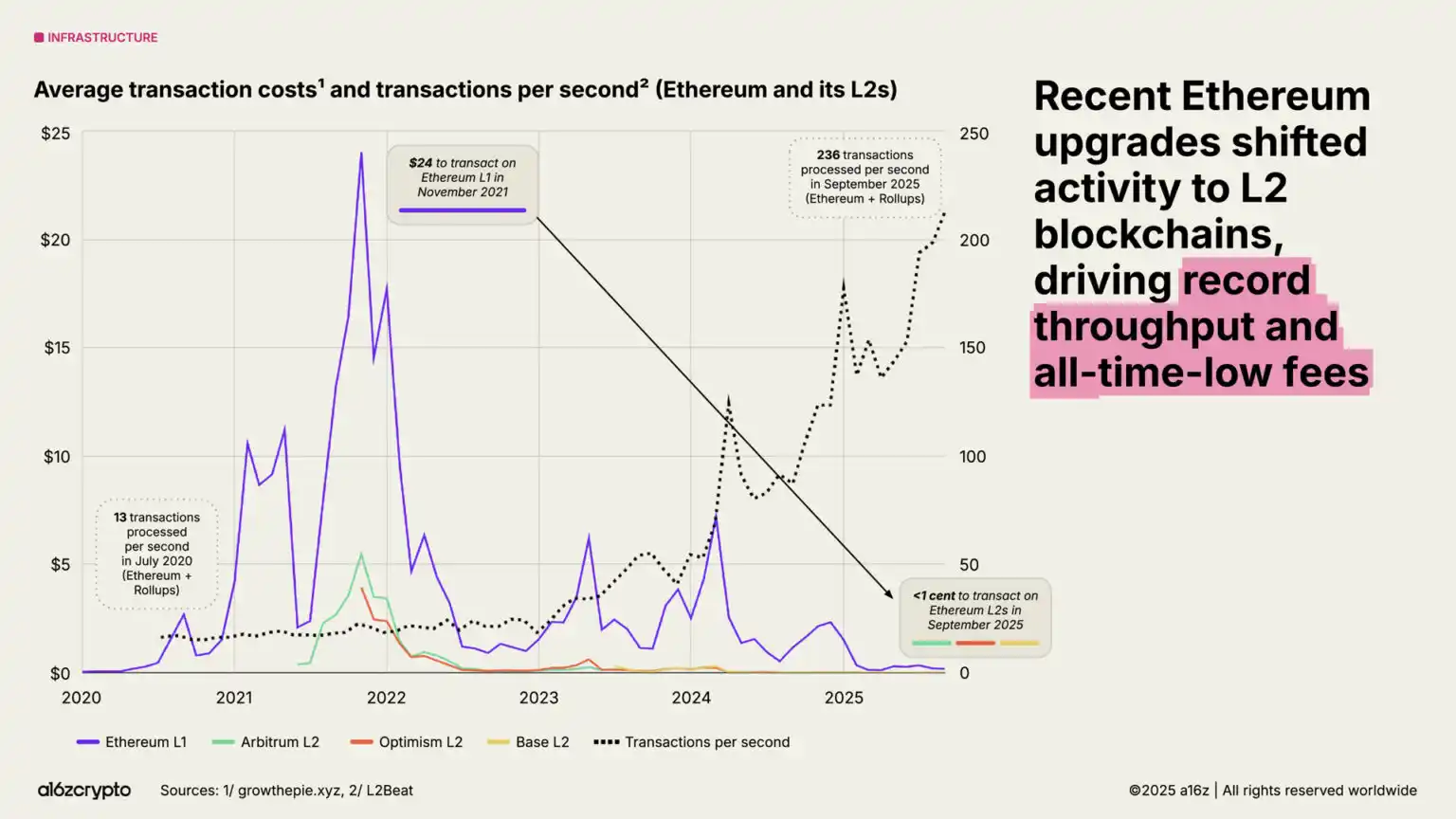

Ethereum continues to advance its scaling roadmap, with most economic activity migrated to second-layer solutions such as Arbitrum, Base, and Optimism. The average transaction cost on L2 has decreased from around $24 in 2021 to less than one cent today, making Ethereum-related block space both cheap and abundant.

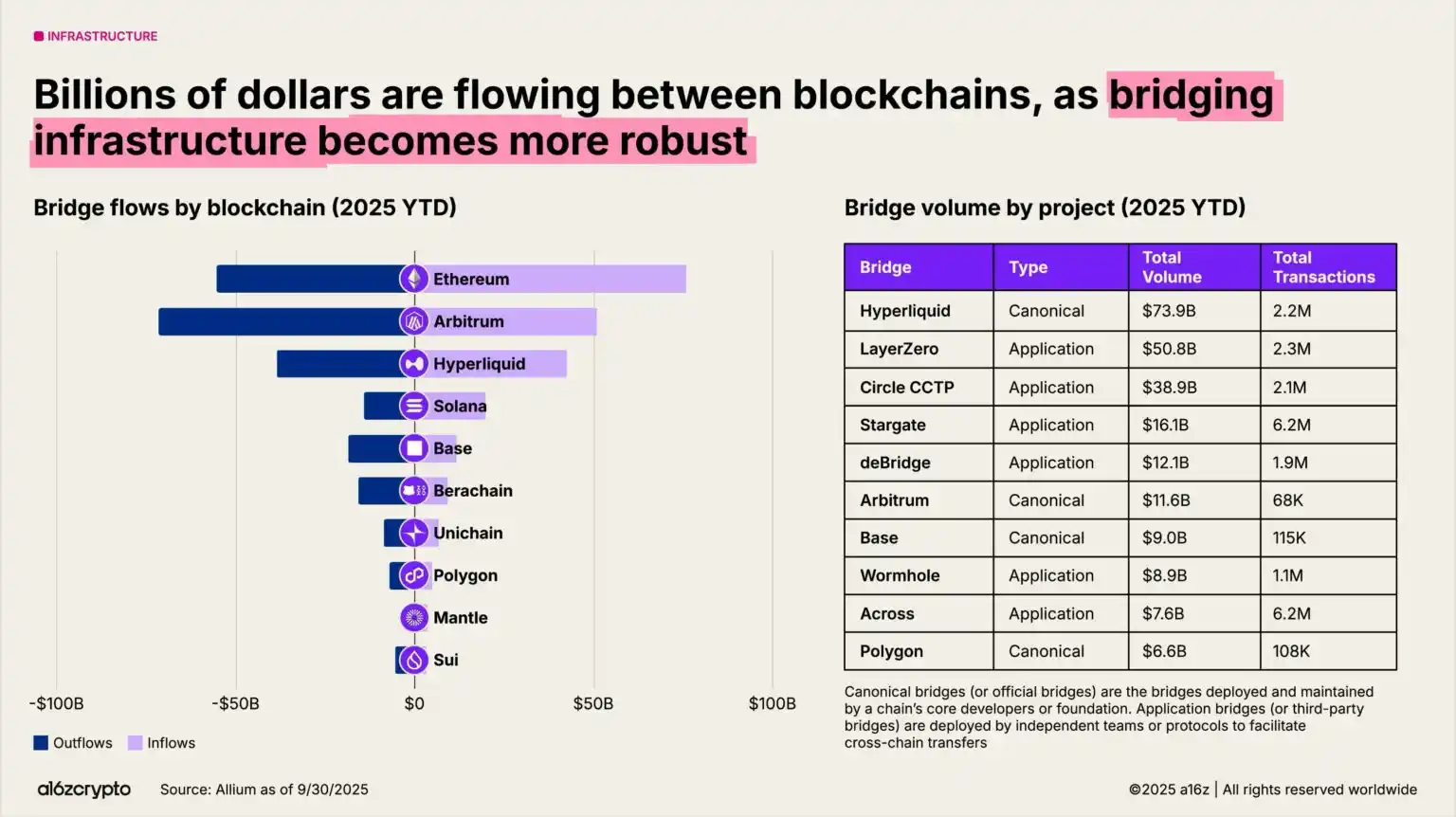

Cross-chain bridges are now achieving blockchain interoperability. Solutions like LayerZero and Circle's cross-chain transfer protocol allow users to transfer assets across multi-chain systems. The Hyperliquid bridge has seen a transaction volume of $74 billion since the beginning of the year.

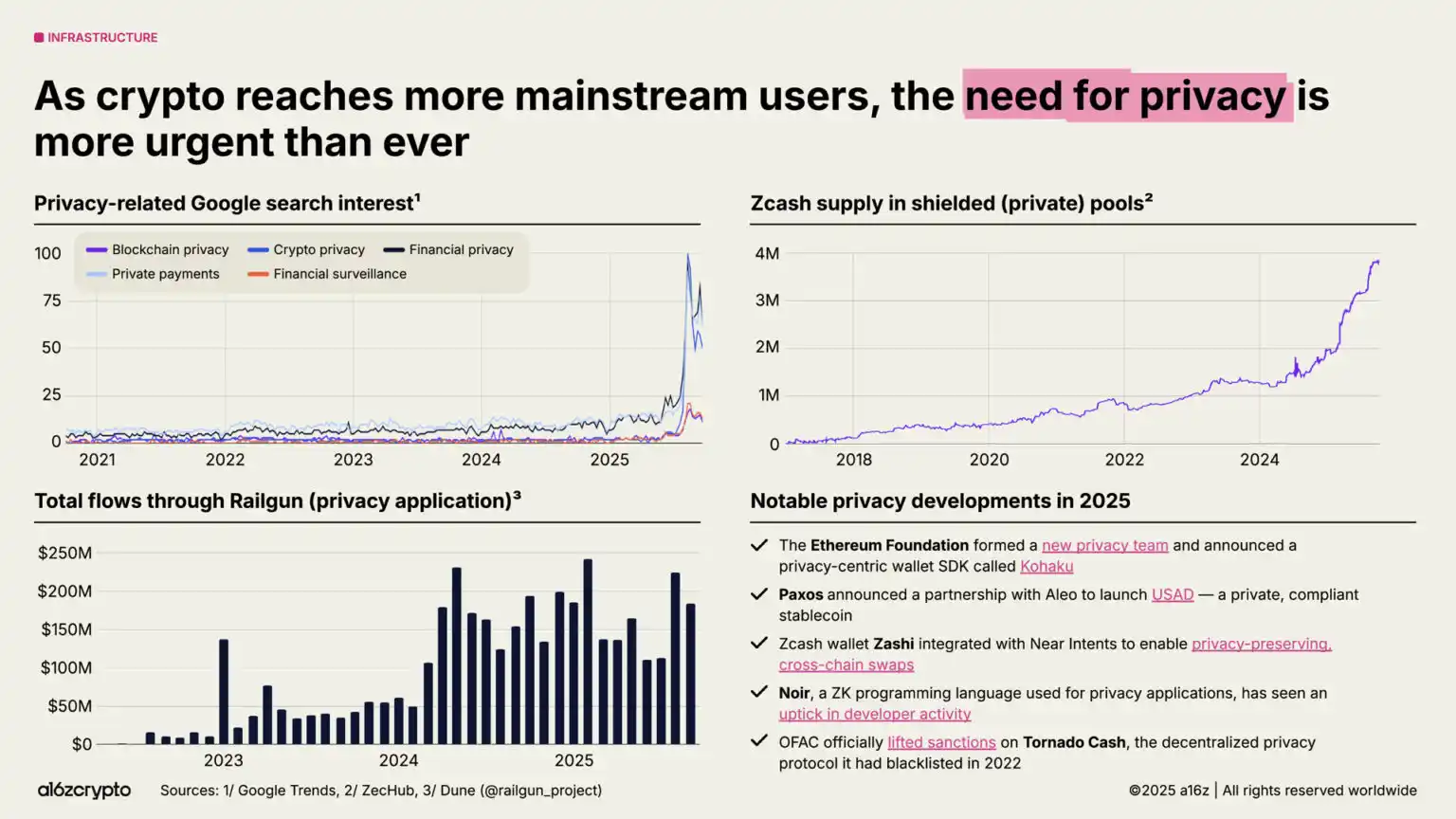

Privacy protection is returning to the forefront and may become a prerequisite for widespread applications. Signs of increased attention include a surge in Google searches related to crypto privacy in 2025; Zcash's shielded fund pool supply growing to nearly 4 million ZEC; and Railgun's monthly transaction volume surpassing $200 million.

More Signs of Development Momentum: Ethereum Foundation has established a new Privacy Team; Paxos collaborates with Aleo to launch a private and compliant stablecoin (USAD); the Office of Foreign Asset Control has lifted sanctions on the decentralized privacy protocol Tornado Cash. We expect that as cryptographic technology continues to mainstream, this trend will gain further momentum in the coming years.

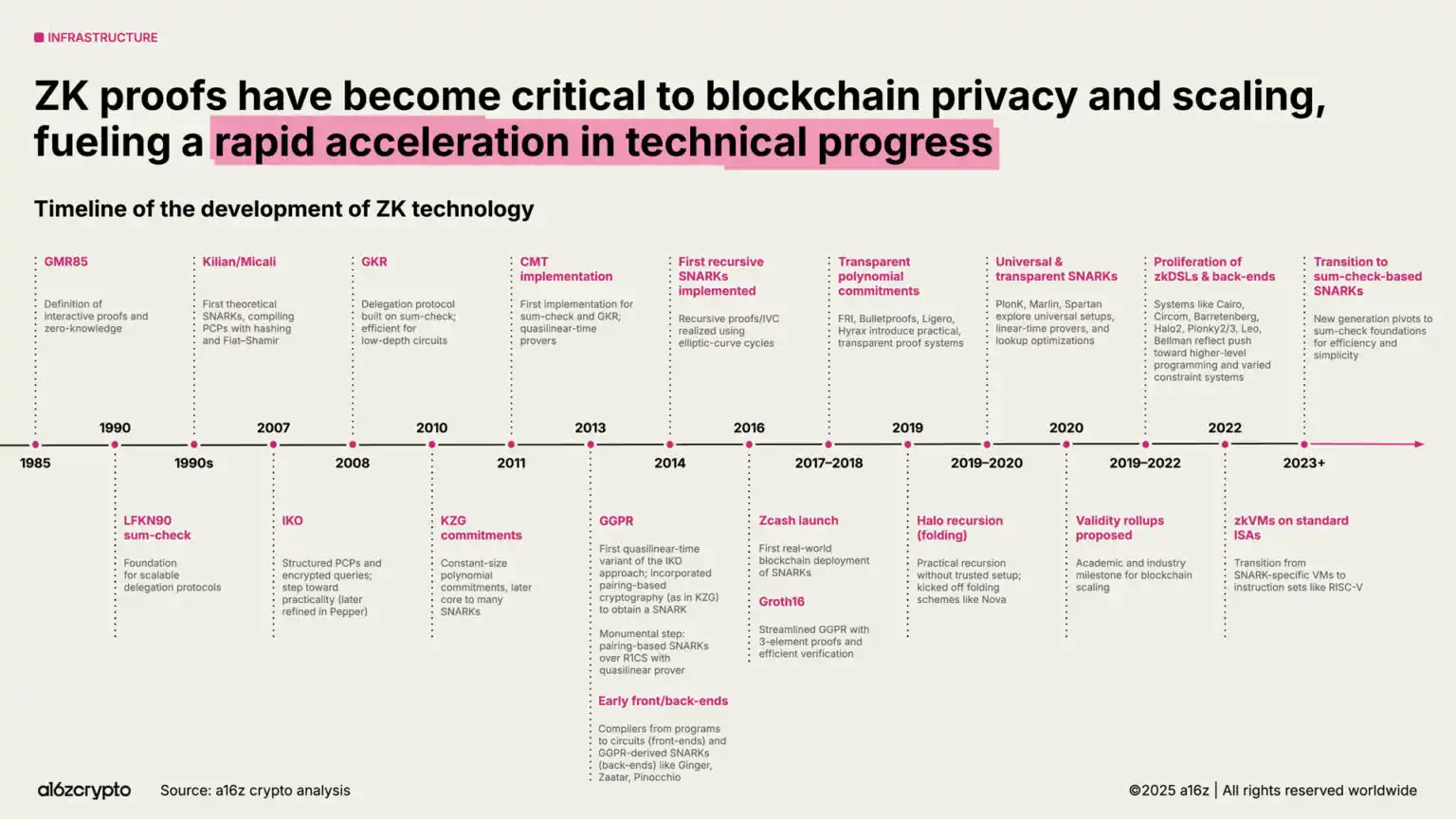

Likewise, zero-knowledge proofs and succinct proof systems are rapidly evolving from decades of academic research into critical infrastructure. Zero-knowledge systems are now integrated into Rollups, compliance tools, and even mainstream web services—a prime example being Google's newly launched ZK identity system.

Meanwhile, blockchain is accelerating progress on the post-quantum computing roadmap. Currently, around $750 billion worth of Bitcoin is held in addresses vulnerable to future quantum attacks. The U.S. government plans to transition the federal systems to post-quantum cryptographic algorithms by 2035.

7. Deep Integration of Cryptography and Artificial Intelligence Technologies

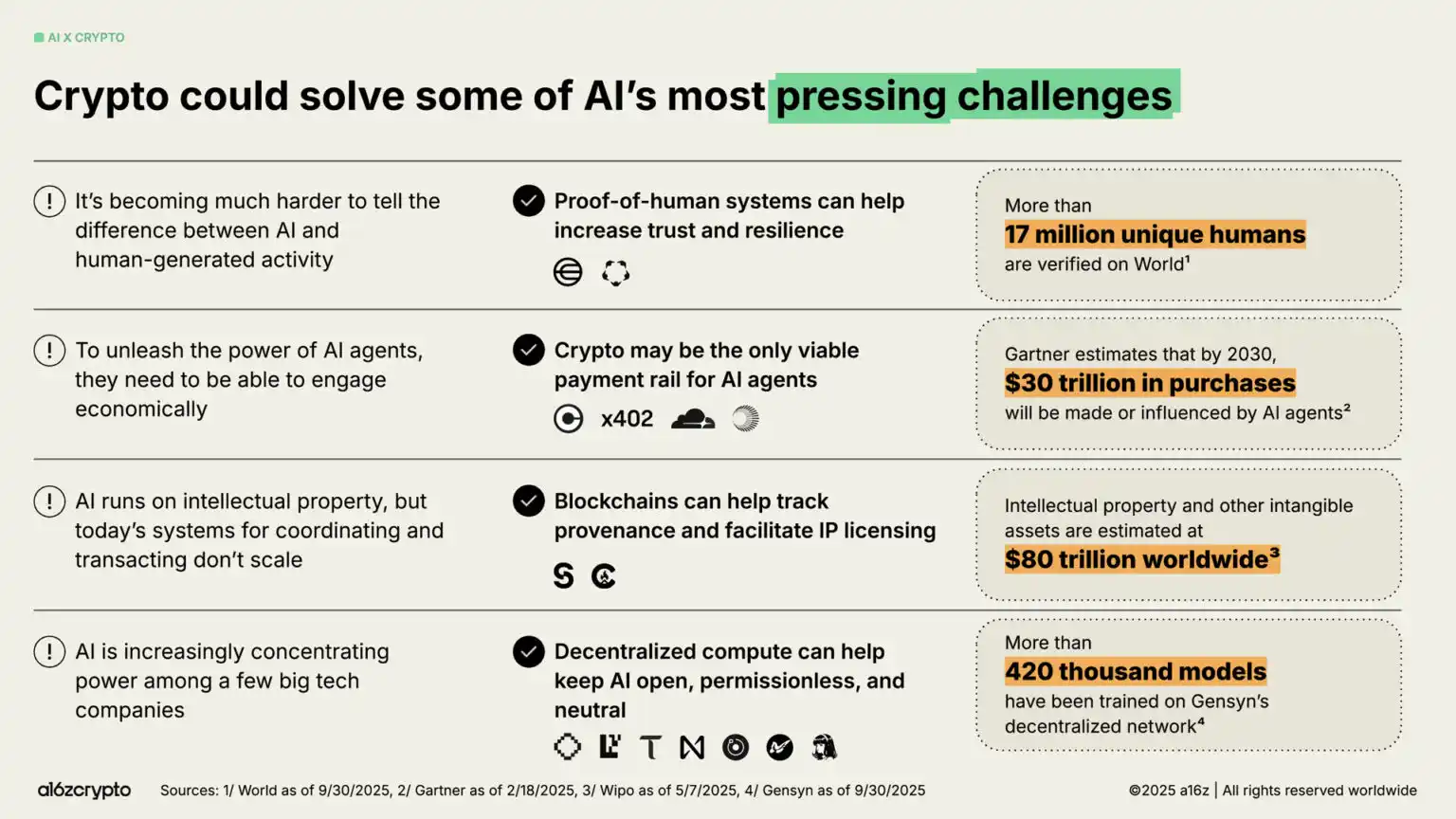

Among many technological advances, the launch of ChatGPT in 2022 has brought AI into the public spotlight—also presenting clear opportunities for the encryption field. From traceability and IP licensing to providing payment channels for intelligent agents, cryptographic technology could be the answer to addressing the most pressing challenges in the AI domain.

Decentralized identity systems like Worldcoin, which have already verified over 17 million users, can provide "human-proof" and help distinguish real users from bots.

Emerging protocol standards such as x402 are becoming potential financial infrastructure for autonomous AI agents, aiding them in microtransactions, API calls, and intermediary-free settlements—Gartner predicts that such an economy could reach $30 trillion by 2030.

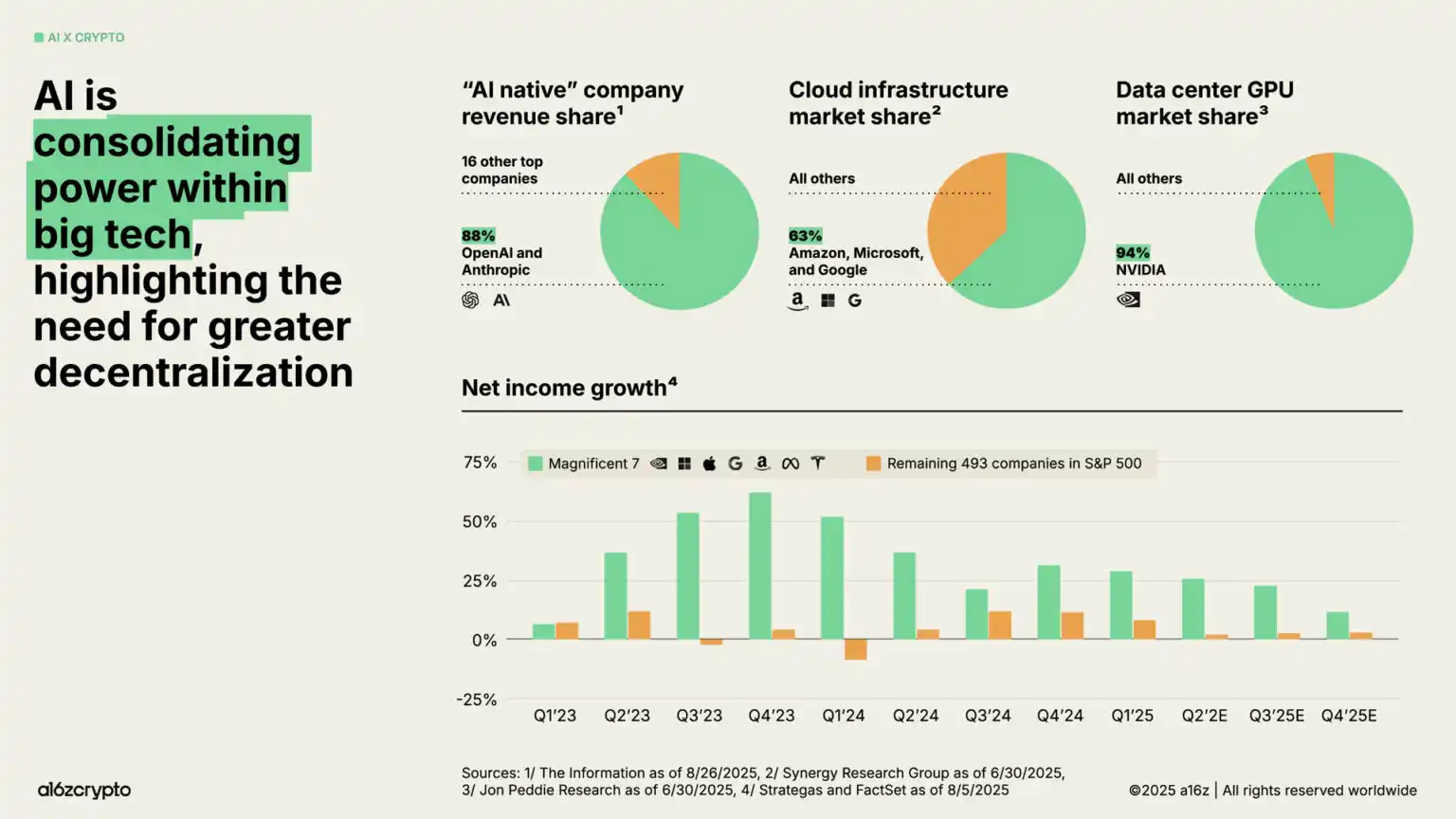

Meanwhile, the computational layer of artificial intelligence is consolidating around a few tech giants, raising concerns about centralization and scrutiny. Currently, only two companies, OpenAI and Anthropic, control 88% of "AI-native" enterprise revenue, Amazon, Microsoft, and Google occupy 63% of the cloud infrastructure market share, and Nvidia holds a 94% share of the data center GPU market. This imbalance has enabled the "Big Seven" companies to achieve double-digit net profit growth for several quarters, while the remaining 493 companies in the S&P 500 have generally failed to outperform inflation.

The blockchain technology provides a counterbalance to the centralizing forces that AI systems exhibit.

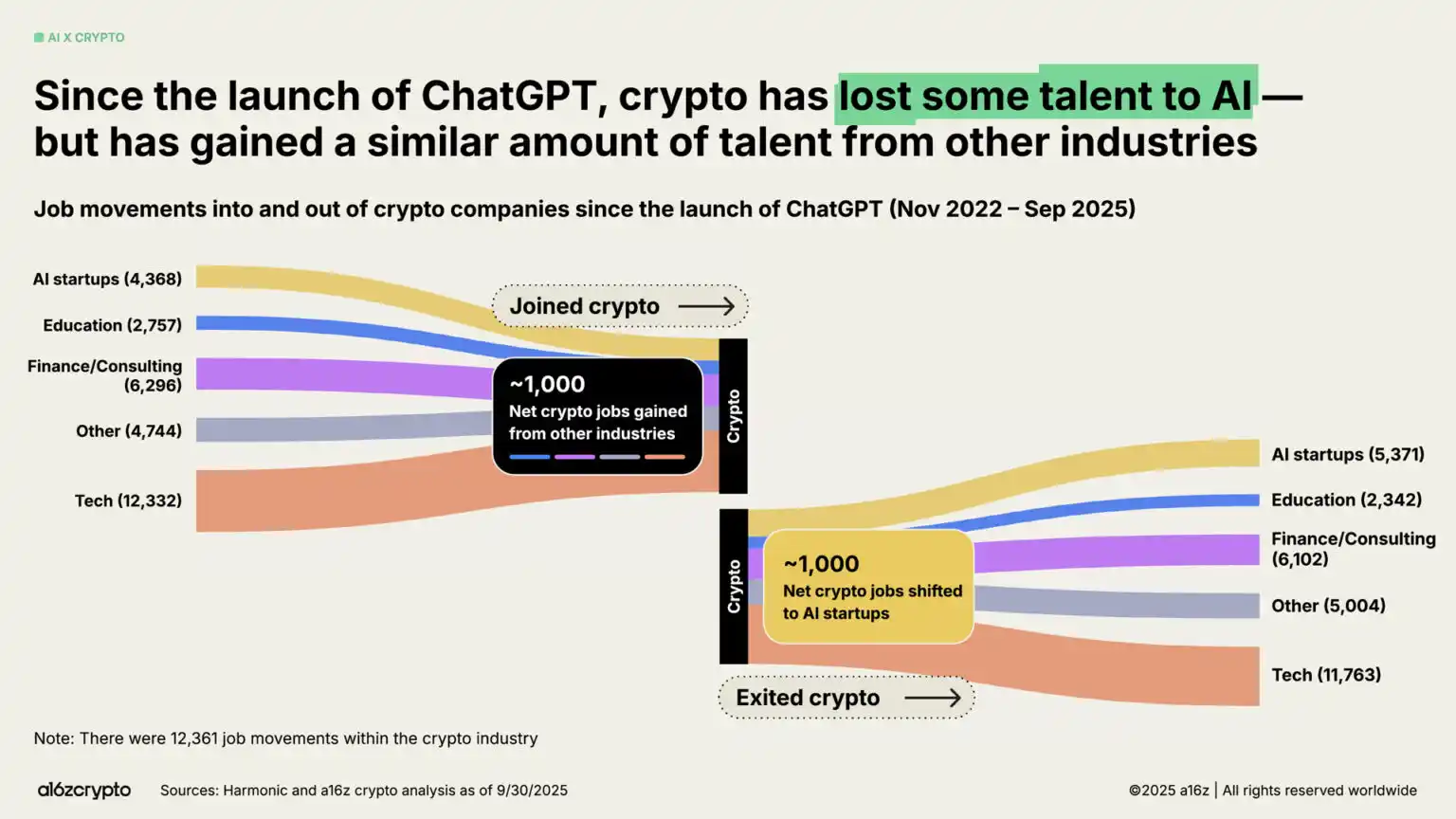

Within the AI hype, some crypto builders have shifted their focus. Our analysis shows that around 1000 roles have moved from the crypto industry to the AI field since the release of ChatGPT. However, this loss has been offset by an equal number of builders joining the crypto industry from traditional finance, tech, and other sectors.

8. Future Outlook

Where are we currently positioned? With regulatory frameworks becoming clearer, the path for tokens to generate real income through fees is becoming evident. The adoption of crypto by traditional finance and fintech will continue to accelerate; stablecoins will upgrade the traditional financial system and drive global financial inclusion; new products will lead the next wave of users into the on-chain world.

We now have the infrastructure and distribution networks in place and are poised to soon gain regulatory certainty to drive the mainstreaming of the technology. It is now the moment to upgrade the financial system, rebuild global payment channels, and shape the ideal form of the internet.

The crypto industry, after seventeen years of development, is bidding farewell to its adolescence and entering maturity.

You may also like

WEEX LALIGA Partnership 2026: Where Football Excellence Meets Crypto Innovation

WEEX becomes official crypto exchange partner of LALIGA in Hong Kong and Taiwan. Discover how this partnership brings together football excellence and trading discipline.

AI Apocalypse, a massive short squeeze

The "Second Truth" of the Luna Crash: Jane Street Exits Ahead of Plunge

Jane Street Market Manipulation, Stripe Considering Acquiring PayPal, What's the Overseas Crypto Community Talking About Today?

WEEX × LALIGA 2026: Trade Crypto, Take Your Shot & Win Official LALIGA Prizes

Unlock shoot attempts through futures trading, spot trading, or referrals. Turn match predictions into structured rewards with BTC, USDT, position airdrops, and LALIGA merchandise on WEEX.

a16z: Why Do AI Agents Need a Stablecoin for B2B Payments?

February 24th Market Key Intelligence, How Much Did You Miss?

Web4.0, perhaps the most needed narrative for cryptocurrency

Some Key News You Might Have Missed Over the Chinese New Year Holiday

Key Market Information Discrepancy on February 24th - A Must-Read! | Alpha Morning Report

$1,500,000 Salary Job: How to Achieve with $500 AI?

Bitcoin On-Chain User Attrition at 30%, ETF Hemorrhage at $4.5 Billion: What's Next for the Next 3 Months?

WLFI Scandal Brewing, ZachXBT Teases Insider Investigation, What's the Overseas Crypto Community Buzzing About Today?

Debunking the AI Doomsday Myth: Why Establishment Inertia and the Software Wasteland Will Save Us

Editor's Note: Citrini7's cyberpunk-themed AI doomsday prophecy has sparked widespread discussion across the internet. However, this article presents a more pragmatic counter perspective. If Citrini envisions a digital tsunami instantly engulfing civilization, this author sees the resilient resistance of the human bureaucratic system, the profoundly flawed existing software ecosystem, and the long-overlooked cornerstone of heavy industry. This is a frontal clash between Silicon Valley fantasy and the iron law of reality, reminding us that the singularity may come, but it will never happen overnight.

The following is the original content:

Renowned market commentator Citrini7 recently published a captivating and widely circulated AI doomsday novel. While he acknowledges that the probability of some scenes occurring is extremely low, as someone who has witnessed multiple economic collapse prophecies, I want to challenge his views and present a more deterministic and optimistic future.

In 2007, people thought that against the backdrop of "peak oil," the United States' geopolitical status had come to an end; in 2008, they believed the dollar system was on the brink of collapse; in 2014, everyone thought AMD and NVIDIA were done for. Then ChatGPT emerged, and people thought Google was toast... Yet every time, existing institutions with deep-rooted inertia have proven to be far more resilient than onlookers imagined.

When Citrini talks about the fear of institutional turnover and rapid workforce displacement, he writes, "Even in fields we think rely on interpersonal relationships, cracks are showing. Take the real estate industry, where buyers have tolerated 5%-6% commissions for decades due to the information asymmetry between brokers and consumers..."

Seeing this, I couldn't help but chuckle. People have been proclaiming the "death of real estate agents" for 20 years now! This hardly requires any superintelligence; with Zillow, Redfin, or Opendoor, it's enough. But this example precisely proves the opposite of Citrini's view: although this workforce has long been deemed obsolete in the eyes of most, due to market inertia and regulatory capture, real estate agents' vitality is more tenacious than anyone's expectations a decade ago.

A few months ago, I just bought a house. The transaction process mandated that we hire a real estate agent, with lofty justifications. My buyer's agent made about $50,000 in this transaction, while his actual work — filling out forms and coordinating between multiple parties — amounted to no more than 10 hours, something I could have easily handled myself. The market will eventually move towards efficiency, providing fair pricing for labor, but this will be a long process.

I deeply understand the ways of inertia and change management: I once founded and sold a company whose core business was driving insurance brokerages from "manual service" to "software-driven." The iron rule I learned is: human societies in the real world are extremely complex, and things always take longer than you imagine — even when you account for this rule. This doesn't mean that the world won't undergo drastic changes, but rather that change will be more gradual, allowing us time to respond and adapt.

Recently, the software sector has seen a downturn as investors worry about the lack of moats in the backend systems of companies like Monday, Salesforce, Asana, making them easily replicable. Citrini and others believe that AI programming heralds the end of SaaS companies: one, products become homogenized, with zero profits, and two, jobs disappear.

But everyone overlooks one thing: the current state of these software products is simply terrible.

I'm qualified to say this because I've spent hundreds of thousands of dollars on Salesforce and Monday. Indeed, AI can enable competitors to replicate these products, but more importantly, AI can enable competitors to build better products. Stock price declines are not surprising: an industry relying on long-term lock-ins, lacking competitiveness, and filled with low-quality legacy incumbents is finally facing competition again.

From a broader perspective, almost all existing software is garbage, which is an undeniable fact. Every tool I've paid for is riddled with bugs; some software is so bad that I can't even pay for it (I've been unable to use Citibank's online transfer for the past three years); most web apps can't even get mobile and desktop responsiveness right; not a single product can fully deliver what you want. Silicon Valley darlings like Stripe and Linear only garner massive followings because they are not as disgustingly unusable as their competitors. If you ask a seasoned engineer, "Show me a truly perfect piece of software," all you'll get is prolonged silence and blank stares.

Here lies a profound truth: even as we approach a "software singularity," the human demand for software labor is nearly infinite. It's well known that the final few percentage points of perfection often require the most work. By this standard, almost every software product has at least a 100x improvement in complexity and features before reaching demand saturation.

I believe that most commentators who claim that the software industry is on the brink of extinction lack an intuitive understanding of software development. The software industry has been around for 50 years, and despite tremendous progress, it is always in a state of "not enough." As a programmer in 2020, my productivity matches that of hundreds of people in 1970, which is incredibly impressive leverage. However, there is still significant room for improvement. People underestimate the "Jevons Paradox": Efficiency improvements often lead to explosive growth in overall demand.

This does not mean that software engineering is an invincible job, but the industry's ability to absorb labor and its inertia far exceed imagination. The saturation process will be very slow, giving us enough time to adapt.

Of course, labor reallocation is inevitable, such as in the driving sector. As Citrini pointed out, many white-collar jobs will experience disruptions. For positions like real estate brokers that have long lost tangible value and rely solely on momentum for income, AI may be the final straw.

But our lifesaver lies in the fact that the United States has almost infinite potential and demand for reindustrialization. You may have heard of "reshoring," but it goes far beyond that. We have essentially lost the ability to manufacture the core building blocks of modern life: batteries, motors, small-scale semiconductors—the entire electricity supply chain is almost entirely dependent on overseas sources. What if there is a military conflict? What's even worse, did you know that China produces 90% of the world's synthetic ammonia? Once the supply is cut off, we can't even produce fertilizer and will face famine.

As long as you look to the physical world, you will find endless job opportunities that will benefit the country, create employment, and build essential infrastructure, all of which can receive bipartisan political support.

We have seen the economic and political winds shifting in this direction—discussions on reshoring, deep tech, and "American vitality." My prediction is that when AI impacts the white-collar sector, the path of least political resistance will be to fund large-scale reindustrialization, absorbing labor through a "giant employment project." Fortunately, the physical world does not have a "singularity"; it is constrained by friction.

We will rebuild bridges and roads. People will find that seeing tangible labor results is more fulfilling than spinning in the digital abstract world. The Salesforce senior product manager who lost a $180,000 salary may find a new job at the "California Seawater Desalination Plant" to end the 25-year drought. These facilities not only need to be built but also pursued with excellence and require long-term maintenance. As long as we are willing, the "Jevons Paradox" also applies to the physical world.

The goal of large-scale industrial engineering is abundance. The United States will once again achieve self-sufficiency, enabling large-scale, low-cost production. Moving beyond material scarcity is crucial: in the long run, if we do indeed lose a significant portion of white-collar jobs to AI, we must be able to maintain a high quality of life for the public. And as AI drives profit margins to zero, consumer goods will become extremely affordable, automatically fulfilling this objective.

My view is that different sectors of the economy will "take off" at different speeds, and the transformation in almost all areas will be slower than Citrini anticipates. To be clear, I am extremely bullish on AI and foresee a day when my own labor will be obsolete. But this will take time, and time gives us the opportunity to devise sound strategies.

At this point, preventing the kind of market collapse Citrini imagines is actually not difficult. The U.S. government's performance during the pandemic has demonstrated its proactive and decisive crisis response. If necessary, massive stimulus policies will quickly intervene. Although I am somewhat displeased by its inefficiency, that is not the focus. The focus is on safeguarding material prosperity in people's lives—a universal well-being that gives legitimacy to a nation and upholds the social contract, rather than stubbornly adhering to past accounting metrics or economic dogma.

If we can maintain sharpness and responsiveness in this slow but sure technological transformation, we will eventually emerge unscathed.

Source: Original Post Link

Have Institutions Finally 'Entered Crypto,' but Just to Vampire?

A $2 Trillion Denouement: The AI-Driven Global Economic Crisis of 2028

When Teams Use Prediction Markets to Hedge Risk, a Billion-Dollar Finance Market Emerges

Cryptocurrency Market Overview and Emerging Trends

Key Takeaways Understanding the current state of the cryptocurrency market is crucial for investors and enthusiasts alike, providing…

WEEX LALIGA Partnership 2026: Where Football Excellence Meets Crypto Innovation

WEEX becomes official crypto exchange partner of LALIGA in Hong Kong and Taiwan. Discover how this partnership brings together football excellence and trading discipline.

AI Apocalypse, a massive short squeeze

The "Second Truth" of the Luna Crash: Jane Street Exits Ahead of Plunge

Jane Street Market Manipulation, Stripe Considering Acquiring PayPal, What's the Overseas Crypto Community Talking About Today?

WEEX × LALIGA 2026: Trade Crypto, Take Your Shot & Win Official LALIGA Prizes

Unlock shoot attempts through futures trading, spot trading, or referrals. Turn match predictions into structured rewards with BTC, USDT, position airdrops, and LALIGA merchandise on WEEX.